Open for Business: the net zero mission

How the UK should capitalise on the transition to net zero to drive inclusive growth

30 August 2023

17 minute read

Summary: In 2018, Britain generated twice as much electricity from wind power as coal. This marked a significant milestone in the rapid decline of the most polluting form of electricity production, buoyed by the UK’s inherent geographic advantages in wind power. However, the economic shocks and increased competition for investment in the global renewable energy sector in the years since have created a continually challenging environment for the UK’s net zero economy. Ensuring that the UK can reap the economic benefits of moving at pace to a net zero economy will require significant supply side intervention. This will include an effective industrial policy, aimed at effectively using the state to build up Britain’s net zero workforce and industry and to demonstrate to investors the massive growth potential of the UK’s green economy.

Recommendations:

- Empower workers and leave no-one behind: Reform the UK’s provision of adult education and training to ensure the UK has the right workforce to capitalise on the opportunity of net zero, while also ensuring that those whose incomes are dependent on the fossil fuel economy are not left behind

- State action and policy certainty: Government intervention to deliver public investment into key infrastructure, with greater certainty in the planning system to lock in private investment

- Demonstrate growth potential: the UK must demonstrate that it can build a viable net zero export market to compete with the US and EU

While there is not yet a clear understanding of just how much investment will be needed to move the global economy to net zero, there is now no doubt that it will require a significant, global capital outlay.

If the UK acts quickly to capitalize on this, it has a real opportunity to build inclusive growth. Infrastructure such as offshore wind, tidal and nuclear power needed to deliver net zero will be hosted in coastal areas.

This means that as well as creating economic growth, the deployment of net zero infrastructure could allow the economy to grow in a more inclusive way. Coastal areas currently lag behind the rest of the UK, with the Social Market Foundation finding that per capita GVA in coastal areas was 26% lower than in non-coastal areas in 2015. Meanwhile a large amount of cheap energy could help to facilitate the growth of UK manufacturing industries, which have been hampered in the past by energy costs higher than those of our competitors.

CPP’s Open for Business series explores the barriers that prevent business investment to support inclusive economic growth. As part of this series, this essay looks at the mounting challenges the UK faces in attracting investment into net zero, while also proposing how the right policy mix can allow the UK to overcome this and to seize the opportunities that net zero offers.

The UK is losing ground in the race to net zero

In the 2010s, the UK was one of Europe’s outright success stories in net zero, notably in the installation of renewable power. Over the decade, Europe saw investments of $719.4bn in renewables (excluding large hydro), of which $126.5bn was invested in the UK. In this period in Europe, only Germany saw a higher level of investment.

However, by the end of the decade and since, this trend has seen a marked shift. In 2019, investments in renewable energy capacity were spread across the continent, with the largest amount of investment going to Spain. This represented a shift with renewable investment diffusing across the continent. While this makes sense, given the need for renewable power sources to cover a broad area, the previous trailblazers in Europe saw a decline in investment as a result. The UK saw a one-year decline on investment in renewables of 40%, with Germany and Italy (the latter seeing the third largest investment in renewables in the 2010s) seeing one-year declines of 30% and 35% respectively.vi

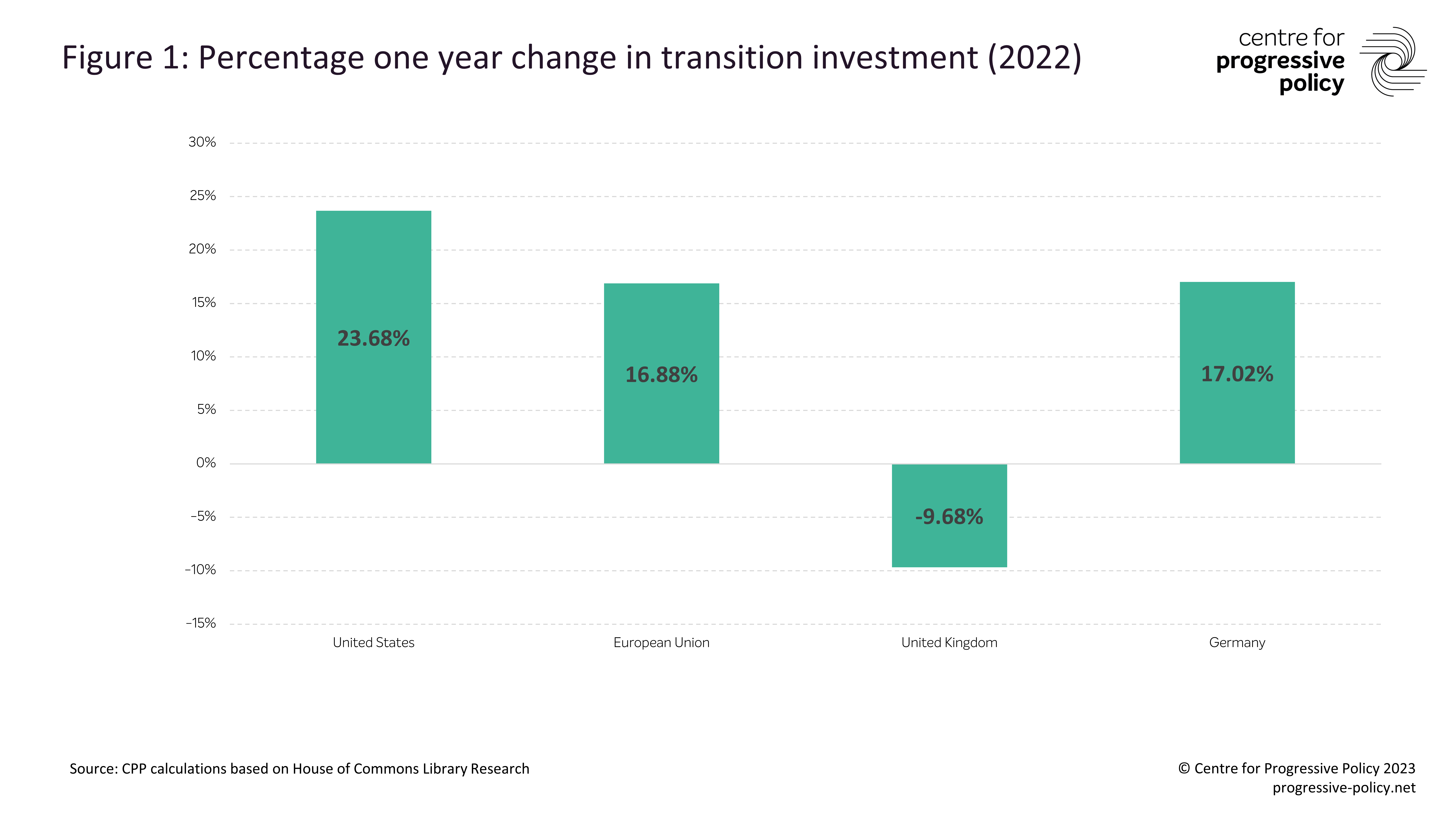

The years since have seen major shocks to the global economy. Following the Covid-19 pandemic, the UK saw a slower increase in energy transition investment than that seen elsewhere in Europe and the USvii. Far more alarmingly, in 2022 the UK saw a fall in net zero investment, even as the US and EU saw significant increases.

The driver of this change seems to primarily have been increased competition. In the aftermath of the invasion of Ukraine, policy makers around the world were forced to rethink energy policy, with a greater emphasis on security and a move away from volatile fossil fuel markets. In the US, the Inflation Reduction Act has dramatically increased the amount of subsidy available for net zero infrastructure, while in response the European Union has launched similar initiatives in the form of RePowerEU and the Green Deal Industrial Plan, to prevent the loss of talent and investment to the US.

Both of these measures have been aimed at increasing subsidies and financial support for the energy transition. As a result, investors have flocked to both jurisdictions in search of government support.

For its part, the UK will struggle to be as generous a destination for investment when it comes to deploying subsidies and direct financial support. Borrowing costs for the UK Government are high, meaning financing support for long term investment will be more difficult than in the US or EU. This has been recognised in the UK, which will struggle to match the sheer amount of money on offer from larger economic blocs. This has been reflected in recent weeks, with senior UK Government figures briefing that “the money just isn’t there” for the UK to make the same kind of intervention in the economy.

This is not to say that the Government has not announced some subsidy measures in the past year. Efforts like the launch of Great British Nuclear and the announcement in the Spring budget of £20bn of investment into carbon capture (over twenty years) represent the UK’s response to these developments. Tata Steel is expected to receive £500mn in return for setting up a gigafactory in the UK. However, the size of the UK’s economy and budgetary pressures mean that the UK will not be able to match the EU and US in a race to the bottom on subsidies. This has begun to worry the UK’s energy industry, with trade group Energy UK beginning a series of work on an emerging 'clean growth gap' between the UK and its peers.

In spite of this, the United Kingdom has distinct natural advantages in the race to net zero. The UK’s geography is well suited to hosting net zero power sources, while its research strengths should enable it to excel at clean tech. However, if it is to attract international investment into these areas, it will need to ensure it has the right policy mix to secure this investment.

Empowering workers and leaving no-one behind

A key aspect of the net zero transition is securing a just transition. The International Labour Organisation defines this as:

“…greening the economy in a way that is as fair and inclusive as possible to everyone concerned, creating decent work opportunities and leaving no one behind”.

This will mean ensuring that those communities currently dependent on the fossil fuel economy see the benefits of a shift to net zero. This will be key, not just to delivering net zero, but to boosting economic growth as a whole. CPP’s model of inclusive growth focuses on how, by getting the economic fundamentals right and seeking to unlock the potential of all people and places, the UK can have a fairer and more sustainable model for economic growth.

While there are obviously major social benefits of ensuring that this happens, there are also major economic reasons for doing so. In a world where capital is highly mobile, investors will seek to align the location of investment to areas where an available workforce matches their skill set. As Professor Riccardo Crescenzi points out in LSE’s Global Investments and Local Development blog, it is types of activity (manufacturing, R&D, headquarters etc) and the stage at which a project sits in the wider value chain that often determines where investment is directed. This is why Formula One teams have based themselves in “motor sport valley” in Oxfordshire and the West Midlands, and why research and development firms set up in university cities.

As with other sectors, attracting investment into the renewable energy sector will require developing a workforce with the necessary skills to deliver net zero. In recent weeks, there has been action taken in this area, with the Government announcing the creation of a Nuclear Skills Taskforce.

Ensuring that the net zero transition promotes inclusive growth means providing retraining opportunities, either through the public or private sectors, or seeking to develop industries that make use of existing skills. There is a clear economic case for doing this. A recent review of the UK’s offshore workforce by Robert Gordon University found that over 90% of the UK’s oil and gas workforce have medium to high skills transferability and are well positioned to work in energy sectors other than oil and gas.

In spite of this, a significant skills gap exists in the UK’s net zero economy. Research by the Place Based Climate Network has found that 6.3million jobs will require significant upskilling for workers who are “in demand”, meaning existing, skilled jobs for which there will be a greater requirement as the UK moves to a net zero economy.

Addressing this challenge will require an overhaul in the UK’s approach to adult education. While the UK has a highly regarded university sector, its overall level of adult education lags behind other countries. In CPP’s recent paper, Open for Business: Unlocking Investment in low-earning economies, we argue that the Government should establish a formal, Prime Ministerial target to raise participation in adult education to 30% by the end of the next Parliament. Further steps, such as the Just Transition Agreements proposed by the businesses and unions behind the Future Energy Skills Programme, could ensure that those working in the fossil fuel sector gain from the opportunities net zero presents. Doing this could allow workers at risk of being left behind by the transition to reskill and enter new industries that emerge as a result of the shift to net zero.

State action and policy certainty

The exact role of the UK state in delivering the transition to net zero is a subject of debate. Much of this has focused on the developing idea of missions, using the government as a coordinating body to drive delivery across sectors of certain goals. In the Open for Businesss report, CPP advocated for a manufacturing mission based on three priorities:

- Boosting productivity

- Supporting environmental sustainability

- Revitalising growth in lagging local economies with robust manufacturing bases

The opportunity to build, install and use more UK based green infrastructure and technology has the potential to drive this growth in local economies and to boost productivity by creating high value added jobs.

There are a few ways this could be achieved. The current Government’s strategy has relied on using initial Government investments to leverage in private sector investment, as seen with the recent announcement of Great British Nuclear.

An alternative approach is to use a publicly owned, arm’s length company, to deliver spare capacity in net zero industries. A version of this has been proposed by Labour, who have proposed creating “Great British Energy” in order to build up renewable capacity. This model has been followed elsewhere, with Norwegian Equinor, French EDF and Swedish Vattenfall all playing a role in upstream energy production. This approach has the advantage of guaranteeing investment into key areas, either through investment by the exchequer, or by using the capacity as a private company to raise capital to make effective, long-term investments in a growth sector.

Delivering a mission-oriented drive towards net zero will involve more than just facilitating and directing investment. The UK has a number of specific obstacles to net zero. The previous section discussed CPP’s proposal for a Prime Ministerial target on adult education. Perhaps as significant a barrier to progress in this space will be the UK’s planning regime, which is in need of significant overhaul if net zero infrastructure (or frankly any infrastructure) is to be built affordably and in good time.

Even setting aside the current restrictions on onshore wind development in England, which has effectively prevented all development, the lengthy delays to getting projects in the ground has been a persistent problem for the UK’s energy sector. A solution that could go some way to addressing this quickly is the National Infrastructure Commission’s call for more regularly updated National Policy Statements for significant infrastructure projects. This would give greater clarity for industry, while also acting to prevent barriers to development by simplifying the planning process.

Growth potential

The final, key driver of investment is the potential of an industry to grow. When a company or institutional investor decides on a new location to set up in, the potential that area has for that investment to grow will play a key role. Under the Growth Share Matrix, a staple of MBA courses, business leaders are taught to seek to invest in projects with the potential for high growth and high market share. It is vital to demonstrate that there is a potential for growth in the UK net zero sector, so that companies see long term prospects as a result of investment.

This is an area where the UK is at a natural disadvantage. If a private company is developing a new piece of net zero infrastructure, adapting it to the larger US marketplace and American regulatory environment will be more lucrative than doing so for the UK.

Fortunately, the UK is in a position where it can avoid this problem by growing the total size of its net zero market. While just hitting net zero is a significant undertaking, the specific geography of the UK means it can, and should, be doing more. The UK has a lot of coastline, in a fairly windy part of the world. The geology of the North Sea could enable the UK to deploy carbon capture and storage. And it sits beside Europe, where major economies like Germany have already announced their hopes of importing hydrogen as they move towards net zero.

This means the UK can have the ambition of growing its net zero sector beyond its own need. Analysis by the UK Business Council for Sustainable Development argues that the UK could unlock as much as £70billion annually in economic development by seeking to become a net exporter of energy.

This growth potential could make the UK a more attractive investment destination. Demonstrating that this is a credible ambition may be trickier. The UK has had two energy security strategies in just the past two years, while recent signals that the Government will backslide on net zero commitments make the UK look uncommitted. If signals from Westminster that the Government are not fully committed to the net zero transition are likely to prompt rethinks on the part of international investors, who are unlikely to be reassured that their industry’s future will remain a priority if the Government flip-flop on green priorities. Proving that becoming a growth market is a priority will require policy makers to develop, and stick to, a credible plan to deliver that mission.

Conclusion: a mission framework for net zero growth

The UK has 7 and 27 years respectively to meet its 2030 and 2050 net zero targets. What happens in the next three decades has the potential to dramatically alter the UK’s economy for the better. With a high skilled workforce and effective investment, the UK could finally overcome its low levels of productivity, growth and pay. Equally, mis-stepping now could see this opportunity lost.

Delivering investment into the net zero economy will require a number of major policy measures. While another energy strategy from Westminster is probably the last thing anyone in the sector wants now, a clear mission framework to address the barriers to this kind of growth should now be a priority. This should include working to deliver a Prime Ministerial target for adult education, as well as removing planning restrictions and intervening to deliver key infrastructure, through partnerships with the private sector and a public owned corporation. It will also require a whole Government approach, with mechanisms like delivery units or cabinet committees set up to drive targets.

If policy makers do this, then far from continuing stagnation, the UK has a real and tangible prospect of securing the benefits that an effective move to net zero can bring.