Abandon fiscal rules to ensure sustainable public finances

26 October 2021

9 minute read

“Public debt is too high. The deficit must come down.”

These are very familiar phrases – calls to action by politicians keen to show off their credibility with the public finances. With the Budget and Spending Review nearly upon us, the same spectre of deficit reduction is haunting the corridors of power on Horse Guards Parade. They will say that the crucial guiding principal for ensuring our future sustainability is to keep a lid on public spending guided by a new set of fiscal rules.[1] It is a self-defeating approach which could leave us as the “sick man of Europe” once again. Instead, fiscal policy should be guided by the twin aims of raising productivity and reducing inequality.

The public debt - household budget fallacy

Governments like to make the analogy between the public finances and household budgets, but this is a fallacy. And it’s a fallacy that results in ad hoc rules of thumb, or worse shock tactics about the potential for future bankruptcy to justify “tough” government spending decisions.

Many economists and policymakers focus on the government’s debt to GDP ratio – the higher the debt burden relative to economic output they say, the less sustainable the government’s finances. Their argument is often that the higher this burden, the greater the interest payments and the harder it will be for government to continue to borrow money. It will eventually make servicing that debt impossible. Much like households, as debt to incomes rise, lenders charge ever higher interest payments and cease providing further loans. The answer to this terrible spiral is to reduce current spending to such an extent that you can start to repay the debt, thereby restoring the confidence of lenders and reducing repayment costs.

To show their commitment to preventing this spiral from happening in the first place, various governments have set out different fiscal rules – all of which are abandoned or significantly altered later. Gordon Brown had his famous Golden Rule which was abandoned in 2009, George Osborne had his budget surplus goal which was ditched in 2016. On the eve of the pandemic there were three fiscal rules: 1. limit public net investment to 3% of GDP 2. ensure the current budget should balance within three years and 3. reassess plans in the event of a pronounced rise in the cost of servicing government debt.[2] But once again these rules were abandoned as government had to respond to Covid-19 with a rapid increase in spending. At the upcoming Budget, Chancellor Rishi Sunak is expected to set out yet another set of rules to rein in UK borrowing and bring down overall debt levels.[3]

But governments are not households. Government spending on education, welfare and health can improve wider society, raising productivity and output, while households mainly spend to consume goods and services for themselves. Governments also have a large capacity to borrow money which households don’t. They can go to the bond market to borrow money, or for those with independent central banks like the UK, they can print money or the central bank can buy up government bonds as happened with quantitative easing. In terms of the bond market itself, there remains plenty of demand for UK government debt which is often called “risk free” because the perceived chance of it defaulting is so low. And while UK debt may have risen during the pandemic, so has debt in every other developed country, with our bonds remaining a safe bet.

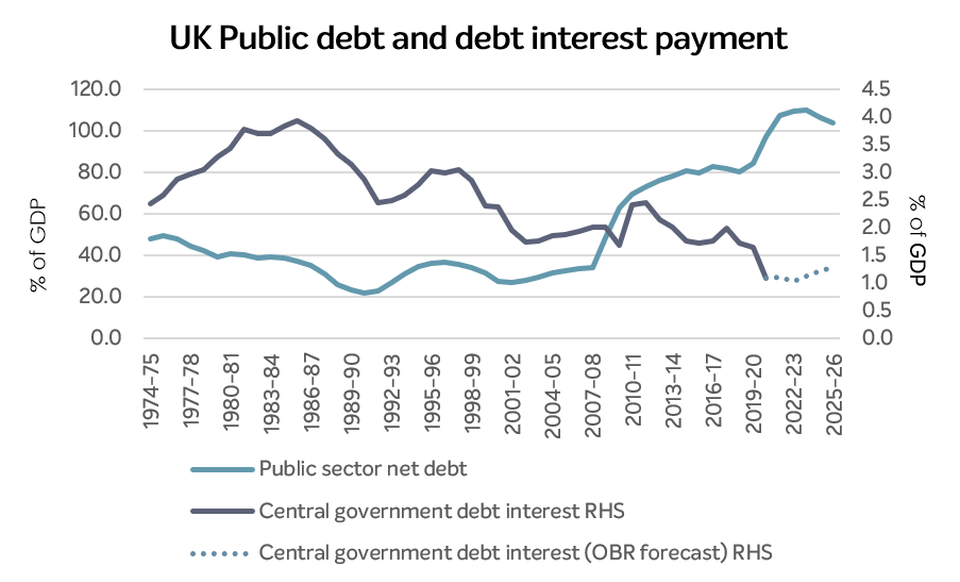

The key point is that while ever increasing government debt might lead to higher debt servicing costs for some countries at some point, this is far from universally true. Japan is the obvious case – its national debt is two and half times larger than its economy and yet its debt interest payments are very low. For the UK too there is no historic relationship between its debt to GDP ratio and the interest payable on its debt. Currently the UK’s debt to GDP ratio is the highest it’s been since WWII and yet the Office for Budget Responsibility (OBR) only forecasts a small rise in debt interest over the rest of this parliament with rates likely to remain low by historical standards (see chart).

At best then, using debt as a proportion of GDP is only a very rough guide as to whether public finances are unsustainable. If there is no clear limit to debt levels, there is limited justification for prioritising stringent short term spending limits over other useful objectives such as boosting productivity or improving welfare.

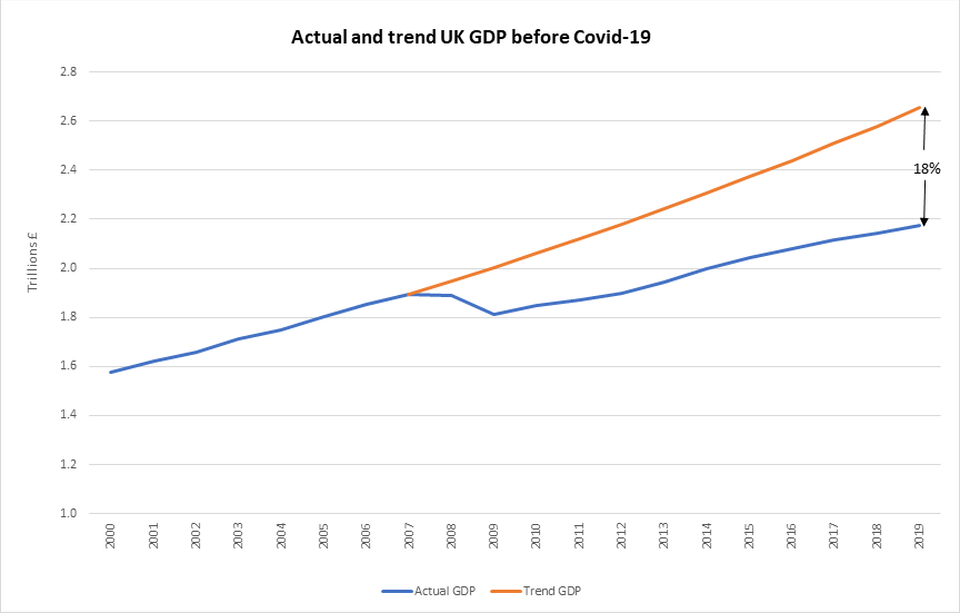

Most importantly of all, the level of debt to GDP is not just driven by spending but the rate of economic growth itself. Looking over the past 20 years, it’s often when the economy has underperformed that governments have abandoned the very rules that were supposed to prove their credibility with the public finances in the first place. As we painfully found out after the financial crisis, a naked focus on cutting public spending did little for the real economy or public finances. By the end of 2019, in the wake of a decade of austerity, the UK’s economy was 18% below the level implied by our pre-financial crisis rate of growth. Or to put it another way it was a whopping £481bn smaller than it should have been. At the same time the government missed its deficit reduction targets time and time again as the economy failed to bring in the expected level of tax revenue.[4]

Abandon short term fiscal rules and focus on the things that matter

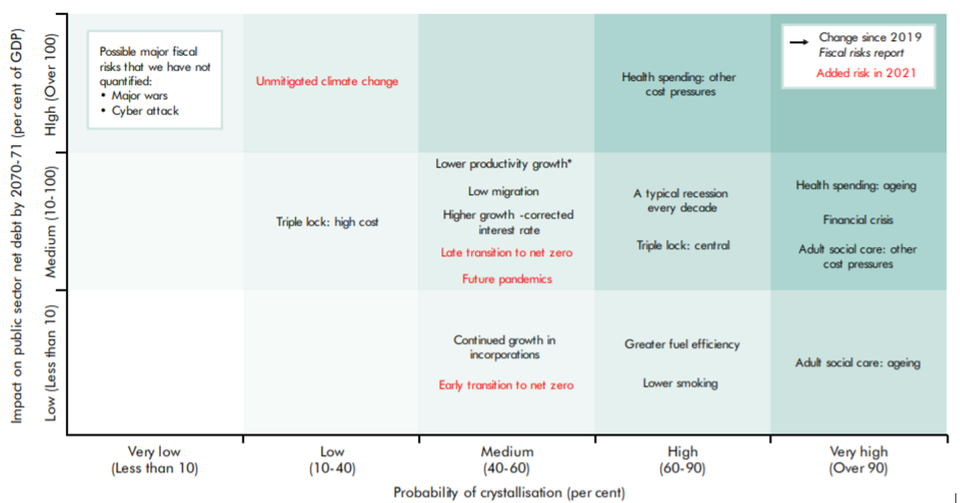

Rather than using ad hoc fiscal rules, or threats about future bankruptcy based on failed household budget analogies to justify spending cuts, responsible government policy should be directed at the biggest issues posing a major long-term risk to our fiscal position. Helpfully, the OBR produces a useful Fiscal Risks report identifying the largest potential long run drivers of rising spending growth and reduced revenue. It turns out that there are three particularly big ills facing us: rising healthcare costs, failed climate change mitigation and slower productivity growth. There are others too, but these are a good place to start.

Sources of risk to fiscal sustainability

Framing the fiscal position around these issues would imply very different policy priorities to deficit reduction underpinned by short term cuts to public services. In fact, in this context, it is far from true that spending cuts to universal credit or local government for instance, would help support our fiscal position. Nor is it clear how limiting increases in the education budget would help. Universal credit helps alleviate poverty which we know is a very important cause of ill health so rising poverty will result in greater spending on the NHS. Similarly, the capacity of local government is important for preventing ill health and it can also be at the forefront of adapting the climate change, but its financial resources have been stripped so bare that its biggest worry is how it can meet immediate adult social care pressures during the winter. And finally, education is critical for developing the human capital this country needs for driving our productivity growth, but despite much talk of substantial investment to help children catch-up after the pandemic, there has been very little additional spend.

Investing in all of these areas is crucial for fiscal sustainability but it will also be important for making a dent in the Conservative’s immediate political priorities of levelling up opportunity and prosperity and moving to a high wage, high growth economy.[5]

Don’t leave it to future generations

Ahead of the upcoming Spending Review, the current government’s strategy appears to amount to spend on the NHS to get waiting lists down, significantly limit spending growth or cut other public services. To its credit, it does have ambitious targets on climate change and has promised added investment, but there is very little in the current plans about how the UK economy can transition to net zero in a fair way that prevents rising inequality.[6]

This position is unsustainable. NHS spending will account for nearly half of day to day government spending by the middle of this decade.[7] The NHS is a vital institution for our nation’s health, but other productive forms of government spending are suffering from a substantial lack of investment. Unless we change course, the UK will be the “sick man of Europe” once again – our economy will flatline and our debt to GDP will rise because we fail to grow productivity, make effective steps to address climate change or reduce the burden of ill health from poverty and rising inequality. This is why the government must prioritise sustainable economic growth and reducing inequality when taking its decisions on tax and spend and not be guided by pointless short-term targets to balance the budget and get the debt down at all costs. Otherwise, we will simply be kicking the can down the road – leaving future governments and generations to deal with a stagnant economy bereft of long-term investment. After a lost decade following the financial crisis, we really cannot afford it.

Notes

[1] https://www.ft.com/content/eb23375d-7219-4b22-a8a7-3060cd848163

[2] https://www.instituteforgovernment.org.uk/explainers/fiscal-rules

[3] Ibid

[4] In November 2016, The OBR wrote: The Government is no longer on course to balance the budget during the current Parliament and has formally dropped this ambition in a significant loosening of its fiscal targets... Confronted by a near-term economic slowdown and a structural deterioration in the public finances, the Government has opted neither for a large near-term fiscal stimulus nor for more austerity over the medium term. https://obr.uk/efo/economic-and-fiscal-outlook-november-2016/

[5] Portes (2021) shows how an immigration strategy alone will not be enough: https://bylinetimes.com/2021/10/18/taking-jobs-or-creating-jobs-the-impact-of-brexit-on-wages/

[6] The Government’s latest plan can be found here: https://www.gov.uk/government/news/uks-path-to-net-zero-set-out-in-landmark-strategy