Changing the rules of the game: a fiscal framework for fair growth

24 July 2023

22 minute read

Summary

Fiscal rules matter for fair growth because they determine how much public money can be borrowed, and what it can be spent on. While democratic accountability and maintaining long term financial stability are perhaps the most compelling arguments for fiscal rules, they are commonly deployed as a show of fiscal credibility, making it easier to borrow from global lenders. Feeling pressured to burnish their credentials on financial stability, the UK Labour party have made fiscal rules a central plank of their policy platform ahead of the 2024 general election, suggesting that they trump all other economic policy priorities. This essay reviews the history of fiscal rules in the UK and reflects on selected international experiences, arguing that strict rules are neither credible or useful in the post-pandemic era. CPP will explore alternatives - including via deliberative research with a citizens jury - and publish our proposals in the autumn.

UK policy context

The UK is in a grim bind. More spending is needed to prevent the collapse of essential public services like the NHS, but debt is high in the wake of the Covid-19 pandemic and the cost of borrowing is rising. To make matters worse, the Bank of England must now push the country towards recession to bring inflation under control, which will only reduce tax revenues while increasing demand on public services. And the UK economy is already underperforming compared to our peers as a result of Brexit, political instability and the underfunding of our health services.[1] Change is desperately needed, but how can it be paid for? This essay continues CPP’s summer series on funding fair growth and considers what role fiscal rules can and should play in shaping the policy environment and providing potential investors with security.

Fiscal rules are defined by the IMF as ‘long-lasting constraints on fiscal policy through numerical limits’ on government budgets and can include limits on levels of government expenditure, deficit debt and tax. They were a major feature of the Labour government under Tony Blair in 1997 which was eager to convince voters of its economic competence after 18 years in opposition. To boost stagnating public investment, Blair’s government adopted a ‘golden rule’ aiming to balance the public sector current budget over the economic cycle and under which borrowing was only permitted for investment in capital like public buildings and equipment. Public debt was also required to be kept below 40% of GDP. These rules held until the financial crisis of 2008-2009 when then Prime Minister Gordon Brown was forced to use taxpayers’ money to buy stakes in strategically important banks to prevent the collapse of the wider banking system. [2] He saved the banks but arguably lost his political credibility and lost the 2010 general election.

The incoming Conservative Chancellor George Osborne revised the UK’s budget balancing and debt rules to meet the new fiscal reality, requiring debt to be declining rather than below 40% GDP and for the ‘cyclically adjusted’ budget to be balanced over a rolling five-year forecast period. [3] He also introduced supplementary targets in 2014 such as a nominal ceiling on welfare spending and more broadly focused on cuts to public spending (austerity) rather than increasing government revenues as the route to balancing the books. Despite loud rhetoric about fiscal prudence, Osborne repeatedly abandoned sets of his fiscal rules during the later years of his chancellorship, with minimal political or financial stability repercussions, undermining the credibility of fiscal rules as a tool for managing the UK economy. [4] In the following years of 2016 to 2020, almost all the government’s numerous fiscal rules ultimately went unmet as spending was first increased in the 2019 spending round and then substantially increased in response to the Covid-19 pandemic. [5]

As in many other countries, the UK’s fiscal rules were suspended in 2020 to enable the government to respond to the Covid-19 pandemic and prevent economic collapse. That fiscal rules across the world have not been able to accommodate large economic shocks has led to calls for them to be replaced with something more flexible, yet in the UK, fiscal rules were reinstated in 2021 without much policy discussion. [6] The limited room that current Chancellor Jeremy Hunt has within our debt rule, led him in the 2023 Spring Budget to, in the words of the Institute for Government, “make some suboptimal choices” around business investment policies and UK government investment in national infrastructure projects such as HS2. [7] This suggests that, despite being intended to do the opposite, our current rules are incentivising short-term decision making at the expense of economic growth.

Yet fiscal rules look set to become even more prominent under Keir Starmer’s Labour party, who are on track to win the next election. In her vision for Britain’s economy, Shadow Chancellor Rachel Reeves makes fiscal rules her first priority and publicly, she has repeatedly reiterated Labour’s commitments to fiscal rules in general and debt rules in particular, saying that the party will not deviate from its commitment for public debt to fall as a share of GDP and that day-to-day spending must be sustainably funded. [8]

The imperative for fiscal rules

So what is the point of fiscal rules and why is Labour so enthused about them? Perhaps most importantly, fiscal rules can be used as a tool for democratic accountability. They provide a benchmark by which commentators and the voting public can judge whether a government is acting responsibly and whether or not voters are being wooed into support at the polling booth with promises of increased spending today at the expense of future parliaments and generations.[9]

Fiscal rules are, however, more readily associated with the connected issue of fiscal discipline. Fiscal rules intend to anchor spending decisions by politicians to long run budget implications and help the Treasury to push back on the spending demand of departments and Number 10, who will always have an incentive to spend more public money to gain political favour. Another imperative for fiscal rules is therefore to convince financial markets and potential creditors of the government’s fiscal credibility: that we are not living beyond our means and it remains safe and attractive to invest in UK government gilts, keeping the cost of government debt down.

This is likely to be a key motivation for Reeves. The history and ongoing perception of the UK Labour as a party of high public spending, brought into relief by Jeremy Corbyn’s 2019 manifesto, contributes to concern that the party is not seen as fiscally credible.[10] In these circumstances, fiscal rules could reduce pressure on government finances if they build market confidence and reduce government borrowing costs.[11]

The spike in yields on 10-year bonds between July and October 2022, from the unstable end of Boris Johnson’s premiership through to the end of Liz Truss’, suggests that political instability and credibility does indeed impact investor confidence.[12] However, the ONS report that the impact of changing yields on borrowing costs is small relative to the impact of inflation. Last December their analysis revealed that steep increases in interest payments on government debt since mid-2021 were largely due to fluctuations in RPI inflation rather than interest rates.[13] This suggests the relationship between fiscal credibility and borrowing costs is not as straightforward as it may seem.

Another question mark over the utility of fiscal rules lies in their widescale abandonment in the wake of the 2020 Covid-19 pandemic and whether or not it is possible to design rules that can accommodate such shocks. If we expect the frequency of large economic shocks to increase as the global climate changes, are fiscal rules valuable if they cannot provide a yardstick for the democratic accountability and fiscal credibility of the government at these such moments?

How do other countries manage their public finances?

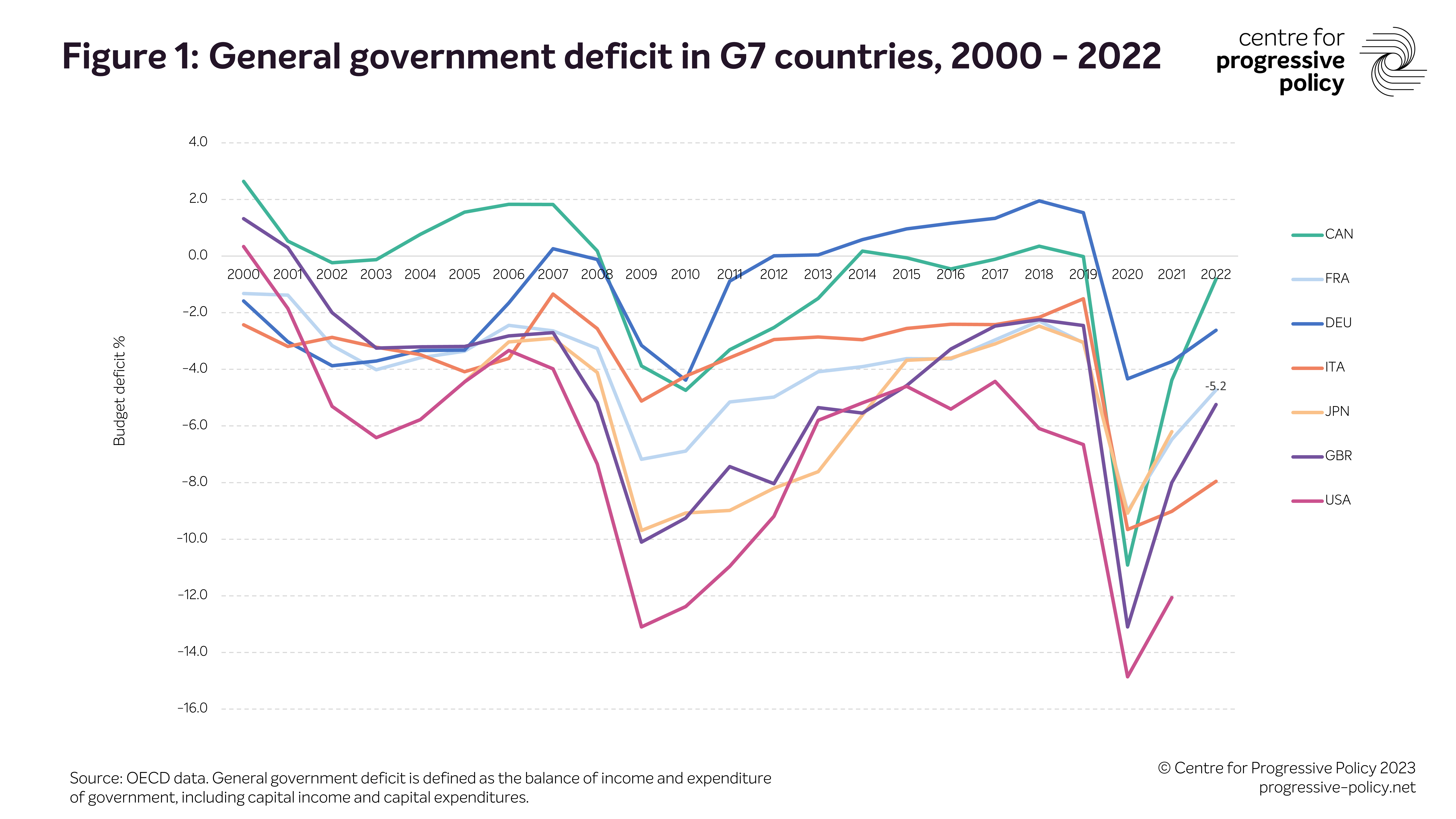

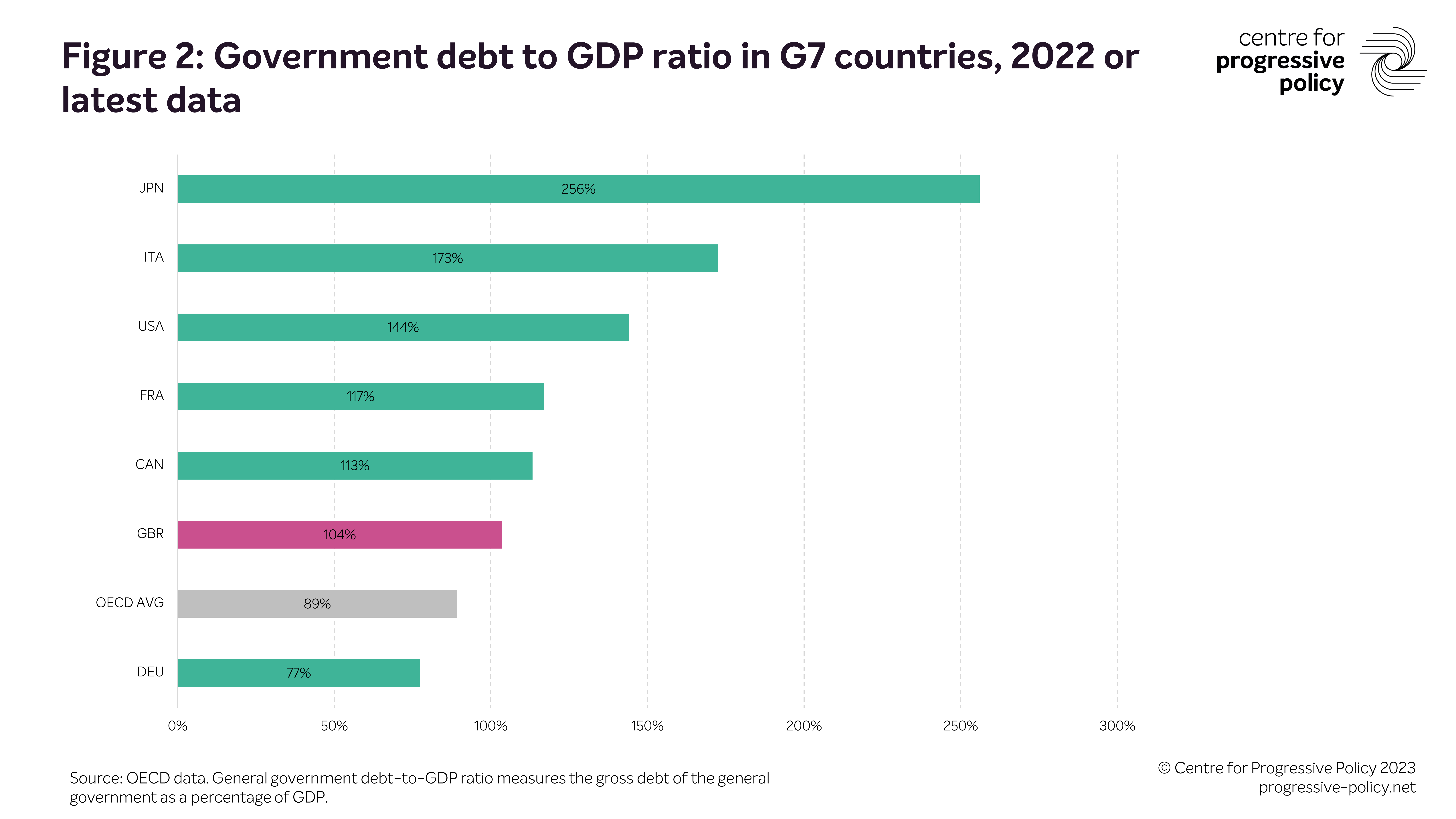

The vast majority of advanced economies have some kind of fiscal rules in place, which set specific restrictions on new expenditure, the budget balance, debt, or taxes.[14] In recent years however, most countries have suspended their fiscal rules and seen levels of public debt rise substantially because of spending during the Covid-19 pandemic which broke out in early 2020. Figure 1 shows a sharp increase in government deficits for G7 countries in 2020 which have not recovered to 2019 levels, in part due to other external pressures on government spending, like the spike in energy prices due to Russia’s war in Ukraine. The UK is currently somewhere in the middle of G7 countries in terms of both its deficit and debt (see Figure 2), although it is worth noting that G7 countries themselves tend to have substantially higher levels of government debt as a proportion of GDP than the OECD average.

Rethinking fiscal rules in the EU

In the EU, the Stability and Growth Pact (SGP) and its fiscal rules apply to all member countries and Euro Area countries are subject to sanctions if they don’t comply.[16] The current rules require countries to keep their budget deficit below 3% of gross domestic product (GDP) and public debt to be below 60% of GDP or diminishing. Like many others, these rules have been suspended since 2020 and are now being reviewed ahead of being reinstated. The European Commission has proposed giving member countries more control over how they meet the fiscal goals to enable gradual debt reduction. This preference for fiscal goals or standards as opposed to hard and fast ‘rules’ is based on the idea that to be credible in an uncertain economic future, fiscal rules must also be flexible, at least at supranational level.[17] The Commission have proposed to issue country-specific recommendations on fiscal policy that are ‘consistent with ensuring that the public debt ratio is put on a downward path or stays at a prudent level and that the budget deficit is below the 3% of GDP reference value over the medium term’ but ‘quantified and differentiated on the basis of Member States' public debt challenges’.[18] This approach has however, met some resistance among EU members. Countries including Germany and the Netherlands have been pushing for clearer and more binding fiscal rules for indebted EU countries, specifically minimum debt reduction requirements.[19]

Sub-national fiscal rules in Italy

Both main political parties in the UK have committed to furthering regional devolution in England and there is growing pressure from existing metropolitan mayors to enable them to keep more of their tax base.[20] Greater fiscal devolution raises the issue of fiscal credibility at a local level and Italy is an interesting comparator here as a G7 country which has had both supra-national (EU) and sub-national rules in place since the 1990s.[21] Local governments in Italy raise over half of their own revenue and are subject to expenditure and debt rules set out in the Domestic Stability Pact (DSP).[22] For example local governments can only carry a deficit to finance investment and must contribute to the national fiscal consolidation effort. However, the European Committee of the Regions reports that “over time, the effectiveness of the DSP in maintaining budgetary discipline has declined due to frequent changes to targets and coverage, which have created uncertainty.” The experience of Italy suggests consistency of targets is important for maintaining buy in from local governments.

The absence of fiscal rules in Canada

Canada also provides an interesting comparator on fiscal rules, because since 2006, it has had none. Instead, they have a Parliamentary Budget Officer (PBO) who is responsible for providing independent economic and financial analysis to Parliament to promote budget transparency and accountability, including on the estimated cost of policy proposals.[23] Stephen Harper’s Progressive Conservative party abolished formal fiscal rules, which had been in place since 1998, on entering office and established the role of Parliamentary Budget Officer to provide independent oversight. This was a response to criticisms around the credibility of the federal government’s fiscal projections and did not signal looser fiscal policy. In fact, in their book, The Harper Factor, economists David Dodge and Richard Dion argue that after 2010, Harper, like many other world leaders including David Cameron in the UK, took a hawkish approach to government finances and even “unduly sacrificed economic growth, in particular public investment, in order to improve a debt position that was already solid”.[24] Constraints on public spending during the period 2010-2017 were much less severe in Canada where spending rose by 0.4% of GDP, than in the UK, where public spending fell by 2.9%.[25] Yet this is likely to be because Canada’s budget balance did not suffer as badly as the UK’s following the financial crisis, rather than because it had looser fiscal policy (see Figure 1). There is nothing in Canada’s experience to suggest that fiscal rules are necessary for achieving fiscal discipline and credibility. Rather, they have adopted innovative and transparent approaches to fiscal discipline such as expanding the PBO’s mandate in 2017 to include non-partisan estimates of the financial cost of election campaign proposals.

Table 1: comparing the UK, Italy and Canada

Country | UK | Italy | Canada |

GDP (US$ per capita)[26] | $55,378 | $51,790 | $57,008 |

Low pay (paid below 2/3 of median) [27] | 16.7% | 3.6% | 19.5% |

Public debt (% GDP) [28] | 104% | 173% | 113% |

Cost of borrowing (10-year gilt yields) [29] | 4.44% | 4.14% | 3.40% |

Budget Deficit [30] | -5.2% | -8.0% | -0.8 |

National Fiscal rules [31] | Budget Balancing Rule, Deficit Rule | Budget Balancing Rule | None |

Subject to supranational rules | No | Yes | No |

Resource rich economy? | No | No | Yes |

Which fiscal rules are most conducive to fair economic growth?

Fair economic growth, that is experienced across the income spectrum and in all places, is key to fiscal sustainability because higher wages and profits mean higher tax revenues. Less poverty also means less demand for costly public services such as income support, housing benefit and services tackling homelessness, child social care and crime. Fiscal rules then, must support widely distributed economic growth in order not to be self-defeating. And as CPP’s Fair Growth model has shown, growth is driven not only by business investment and the presence of high GVA sectors, but by the public services that enable greater participation and productivity in the labour market like childcare, adult skills and preventative health services.[32]

Fair fiscal rules must also enable spending in these areas, particularly in the post-industrial and coastal places across the UK whose local economies have increasingly been lagging behind. Time has shown that these areas will not regenerate on their own and rules that restrict investment risk fuelling political instability and right-wing extremism in places looking for someone to blame, as is happening across Europe.[33]

Amid the complex interplay of public services, industrial strategy, business investment and political stability, strict and simplistic fiscal rules suddenly seem like a rather blunt instrument. Academics at the University of Munich have found empirical evidence that rigid fiscal rules deter public investment and flexible rules increase it, while researchers at the OECD have recognised the inherent trade-offs between fostering economic stability and improving the allocation of resources, concluding that the current economic context poses challenges to fiscal rules’ enforcement and design. [34],[35]

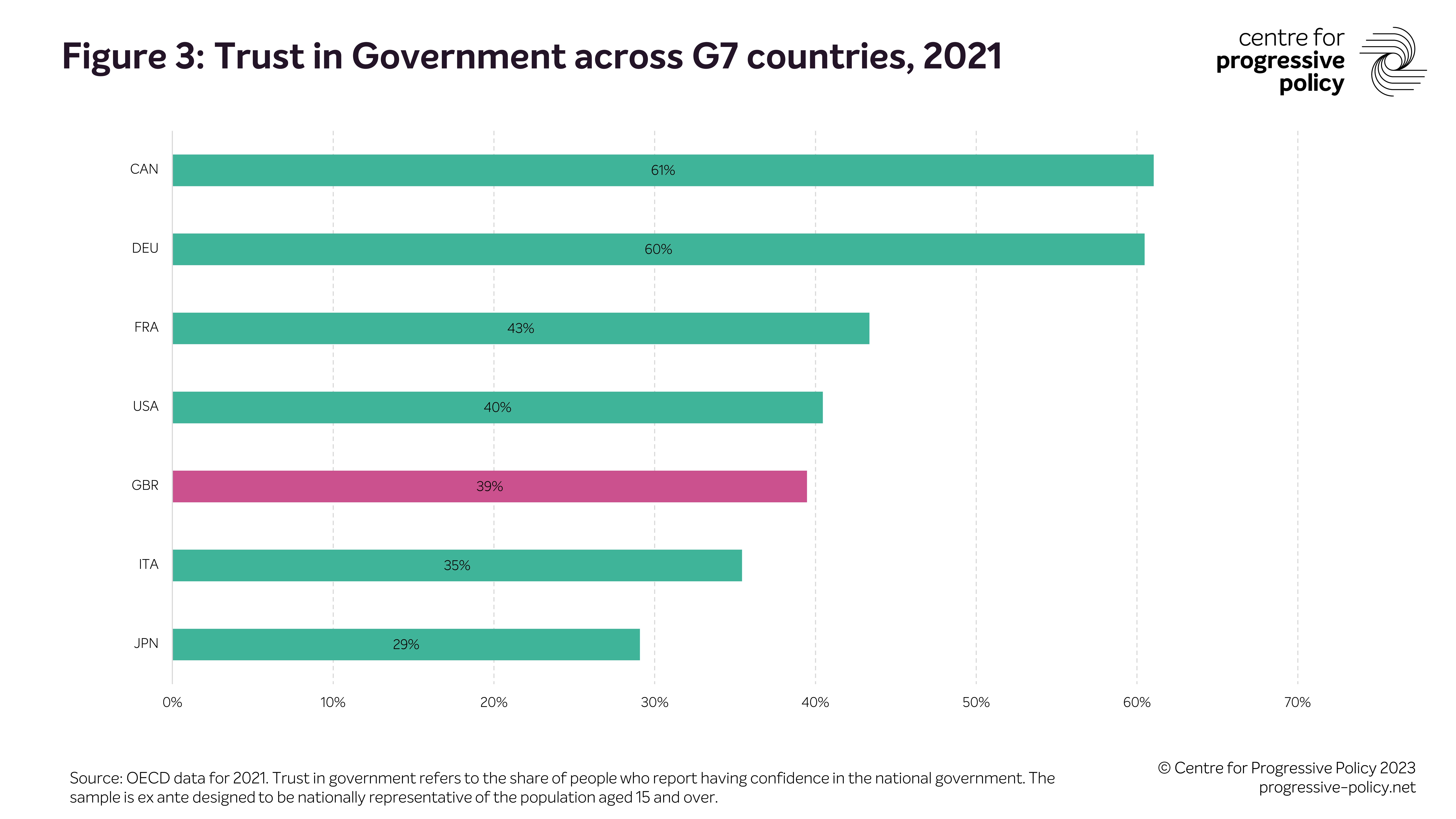

Prioritising strict fiscal rules above all else, as Hunt appeared to do in his 2023 Spring Budget and as Reeves seemingly promises to do if Labour gets into office, risks jeopardising the very objectives fiscal rules seek to achieve. But can something more nuanced be credible? The UK has low levels of trust in government (39.5%) relative to somewhere like Canada (50.7%) which manages to maintain fiscal credibility without legally binding rules.[36] And if it is true that the UK Labour party remains associated with high levels of spending in the public’s mind, looser fiscal standards may make achieving fiscal credibility even more difficult.

Possibilities for reform

Across the economic sphere, the rules are being rewritten. The Covid-19 pandemic saw levels of public spending not seen since World War Two and scientists predict that the probability of such pandemics is increasing.[37] Meanwhile, Europe is weaning itself off Russian gas after Putin’s invasion of Ukraine and the US President Joe Biden has signalled that globalisation is in retreat. In this context, a return to the same old fiscal rules appears to lack ambition and foresight.

So what are the alternative options for anchoring spending decisions to their long term implications and supporting fiscal discipline, credibility and accountability whilst not constraining fair growth or our ability to respond to crises?

Table 2: proposals for new fiscal rules

Suggestion | Detail | Proponent | Advantages | Disadvantages |

Flexible rules-based framework | Long term debt rule and annual deficit rule that has an escape clause and is adjusted based on the cost of borrowing. Goal to increase public net worth to sit alongside fiscal rules. | Tony Blair Institute [38] | Allows more flexibility to stabilise the economy whilst not moving too far from a familiar framework | Maintains deficit and debt rules that can have a distortionary impact on public investment decisions |

Fiscal targets | Focus on a budget balancing target rather than a deficit rule and a public sector net worth target instead of a debt rule. | Resolution Foundation [39] | Reduces incentives for using public investment and asset sales for ‘fiscal fine tuning’ | A novel approach that would require new data and monitoring and require the parties to shift away from debt politically |

Public sector net worth | Base investment decisions on whether they add to the country’s net worth – our assets net of any liabilities such as debt. This could include environmental assets such as Natural Capital or take a more conventional approach and focus on physical infrastructure like hospitals, schools and roads. | Andy Haldane | Enables investment in a new set of public goods needed to meet the challenges of today’s economy. | The scope and definition of public assets needs to be agreed. Risk that fiscal credibility is damaged without other balances in place. |

Former Bank of England Chief Economist Andy Haldane has argued for an asset-based approach, which considers the net impact of government capital spending on the total value of public assets like hospitals, roads, intellectual property and the environment rather than making a decision based purely on financial liabilities. [40] This could help to safeguard the interests of future generations and ensure democratic accountability by actively encouraging public investment that improves the country’s assets. Under this approach, Hunt would have been less likely to delay investment in HS2 at the 2023 Spring Budget, as the transport infrastructure created would have been seen as an asset on the balance sheet as well as a cost to the exchequer. Reaching a balance between assets and liabilities should help to ensure long run credibility however, there is a risk that uncertainty around the valuation of public assets could make it easier to game spending decisions for political gain.

Former Treasury Minister Jim O’Neill also thinks that fiscal rules are currently holding back investment, to the detriment of economic growth. [41] He has voiced support for a simple system that approves investments if they have a positive multiplier and grow the economy. Practically, like the Commission’s proposed ‘fiscal goals’ for the EU, this would mean more reliance on modelling by fiscal councils such as the OBR and may risk politicising their judgements. This risk could be managed by better resourcing the OBR so that they are able to be more directly accountable to Parliament, as the PBO is in Canada, preparing analysis on request for individual Members of Parliament as well as parliamentary committees.

This approach could work within Labour’s current stated fiscal rules whereby day to day spending should be funded via taxation but there is potential to borrow for non-capital investment if the OBR agrees there is evidence it will boost our capacity to grow. For example investing in the childcare system which CPP estimates could add £27bn to the economy. [42] The definition of ‘capital’ could also be broadened to include human capital so that government initiatives to train insulation engineers or early years practitioners for example could be financed from borrowing. This kind of re-classification would require independent oversight from a body like the OBR, perhaps supported by the Office of National Statistics (ONS).

Yet, if the party is wedded to a strict set of fiscal rules, some tweaks might help the rules to promote, rather than prevent, fair growth while continuing to signal Labour is the party prudence. One would be to drop a strict debt rule, or at least expand the time frames during which government must see debt fall, so as not to constrain the investment necessary to boost growth. Another would be to include an escape clause to cover times when GDP is below potential due to a crisis or downturn. Current rules can be suspended if there is a significant negative shock, but the parameters for this are not defined.

Conclusion

Fudging fiscal standards to kick today’s problems into tomorrow risks putting our collective debt on an unsustainable path, increasing the cost of repayments and dragging on the growth of future generations. But neither should strict adherence to spuriously precise rules delay growth-enhancing investment in the UK’s people, places and public services. The ‘rules of the game’ need to change, the question is, how? CPP will be working alongside the National Centre for Social Research to explore this question as part of a citizens jury over the summer and will publish our proposals in the autumn.

Notes

[1] https://mainlymacro.blogspot.com/2023/06/wishful-thinking-on-uk-inflation.html

[2] https://www.theguardian.com/politics/2010/feb/21/gordon-brown-saved-banks

[3] A cyclically adjusted budget calculates what the government's budget deficit would be if the economy was at a normal level of activity, assuming that tax and spend rules and rates are unchanged. It controls for changes to revenue as a result of the business cycle e.g. higher spending on unemployment benefits in a recession.

[4] While Osborne’s fiscal rules mostly remained on track 2010 to 2014, after 2014 they were abandoned on several occasions. See: https://www.instituteforgovernment.org.uk/explainer/fiscal-rules-history ;

[6] https://www.piie.com/publications/working-papers/redesigning-eu-fiscal-rules-rules-standards

[7] https://www.instituteforgovernment.org.uk/comment/jeremy-hunt-spring-budget-2023

[8] https://labourtogether.uk/report/new-business-model-britain

[9] They can also paradoxically do just the opposite: encourage short-termism with a focus on keeping the rule rather than investing in services or growing the economy.

[10]With the Laffer Curve widely discredited, there is little reason that public spending funded through tax rises is necessarily unsustainable.

[12] https://markets.ft.com/data/bonds/tearsheet/summary?s=UK10YG

[14] https://www.imf.org/external/datamapper/fiscalrules/map/map.htm

[15] https://data.oecd.org/gga/general-government-debt.htm

[16] https://www.imf.org/external/datamapper/fiscalrules/map/map.htm

[17] https://www.piie.com/publications/working-papers/redesigning-eu-fiscal-rules-rules-standards

[18] https://ec.europa.eu/commission/presscorner/detail/en/ip_23_1410

[20] https://www.ft.com/content/80920763-6637-4f34-a7b2-ef4cb21992e2

[21] Based on the IMF Fiscal Rules database

[22] https://portal.cor.europa.eu/divisionpowers/Pages/Italy-Fiscal-Powers.aspx

[23] https://www.pbo-dpb.ca/en/about--a-propos

[25] Source: OECD (2020) OECD Social Expenditure database, (www.oecd.org/social/expenditure.htm).

[26] https://data.oecd.org/gdp/gross-domestic-product-gdp.htm

[27] The incidence of low pay refers to the share of workers earning less than two-thirds of median earnings https://data.oecd.org/earnwage/wage-levels.htm#indicator-chart

[28] https://data.oecd.org/gga/general-government-debt.htm

[29] The interest rate required by investors to loan funds to governments. A higher rate implies higher risk and a higher cost of borrowing. https://tradingeconomics.com/united-kingdom/government-bond-yield accessed on 13th July 2023

[30] https://data.oecd.org/gga/general-government-deficit.htm#indicator-chart

[31] https://www.imf.org/external/datamapper/fiscalrules/map/map.htm

[32] https://www.progressive-policy.net/publications/fair-growth

[34] https://www.ifo.de/DocDL/wp-2023-393-blesse-dorn-lay-fiscal-rules-public-investment.pdf

[35] https://read.oecd.org/10.1787/d2798c9e-en?format=pdf

[36] https://data.oecd.org/gga/trust-in-government.htm

[37] https://www.pnas.org/doi/10.1073/pnas.2105482118

[39] https://economy2030.resolutionfoundation.org/wp-content/uploads/2023/03/Cutting_the_cuts.pdf

[40] https://www.ft.com/content/d57567c3-cd97-4cbe-be00-6cf50886b308

[42] https://www.progressive-policy.net/publications/growing-pains