Open for Business: Introducing CPP’s new research programme on business investment

6 February 2023

7 minute read

After months of desperate scrambling for investment to keep the firm afloat, last month reports began circulating that the electric vehicle battery-making startup Britishvolt had finally collapsed. Nearly three hundred staff were immediately made redundant, while the three thousand jobs that the firm was expected to create in its £3.8bn gigafactory based in the Northumbrian coastal town of Blyth were put on indefinite hold. Weeks of uncertainty over the future of the site came to an end only this morning, as news broke confirming that Australian firm Recharge Industries will pursue the Northumbrian gigafactory as its first major project.

As further details emerge over the coming months, more questions will be asked about how Britishvolt - once heralded as the future of the UK automotive sector – struggled to attract investment. But part of the story is already clear. The government had pledged a £100mn investment in recognition of the firm’s potential role as a lynchpin of the UK’s green economy, but had refused to release any investment for the early development of the gigafactory. Rejecting three separate requests for advances worth £30mn, £11.5mn, and £3mn, the government insisted that the investment would only become available once sufficient development of the gigafactory had been made. This made Britishvolt a particularly difficult pitch to private investors who were expected to carry the bulk of the risk in funding its early development. Investors were ultimately unwilling to carry the risk, leading to the firm’s collapse.

It is rarely a surprise when startups fail; the vast majority of them do. But the collapse of Britishvolt has come as a shock to many. How could such a vital part of the UK’s green economy and automotive sector, a company so symbolic of both levelling up and ‘global Britain’, not attract investors? That a firm like Britishvolt should fail to get off the ground suggests that at the heart of this story lie more fundamental questions about how we encourage, and discourage, business investment in different parts of the UK economy. How effective has the UK been at shaping different markets to encourage investment in sectors and places in our economy that are vital for our growth? Who gets investment, who misses out, and what does this suggest about what we place value upon in our economy?

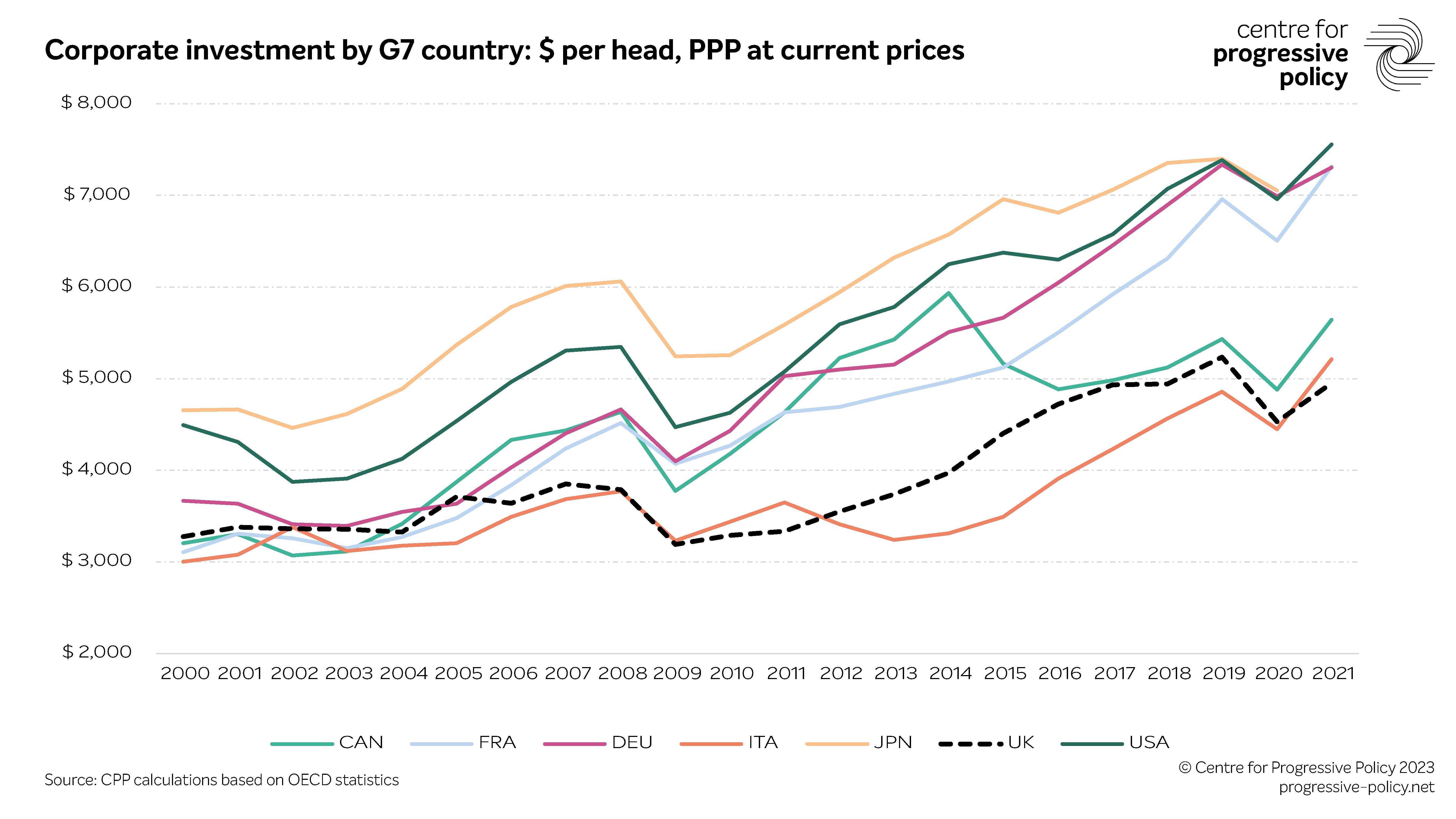

The UK economy has had a particular problem around low levels of business investment for much of the post-war period. It was identified as a central point holding back economic growth in both the National Plan published by the Labour government of 1965, and the Mais Lecture delivered by then-Chancellor Rishi Sunak just last year. As the chart below shows, we lag behind all of our international counterparts on private sector investment – and as a share of GDP it is estimated to have fallen from 14.7% of GDP in 1989 to just 10% in 2019. This is a major factor behind our dismal growth outlook that is now the lowest among G7 economies.

This has had significant economic and social costs. A direct link can be drawn between low levels of business investment and the diminishing living standards of many individuals and communities. As an upcoming paper from CPP will set out later this month, our stagnant productivity growth is highly linked to low levels of investment in capital: tangible, intangible, and human, which has held down real wage growth and contributed to a surge in in-work poverty in recent years.

The UK is also one of the most regionally unbalanced economies in the OECD, which is now widely recognised as a leading drag on growth. This stems largely from our transition into a service-based economy, where private investment favoured high-value, service-oriented firms based overwhelmingly in London and the Greater South East, while many high-productivity, high-growth potential industries based in other parts of the UK struggled to attract investment and scale up. Not only has this held back many of our local economies from developing but it has also dampened their spirit - recent polling conducted by CPP found that those living in so-called “left behind” places are the least optimistic for the future of their local economies.

Successive governments have sought to unlock greater business investment through different financial and regulatory incentives, yet often this has favoured some sectors and places within the economy far more than others. Tax incentives are overwhelmingly targeted towards relief for high-tech, R&D-intensive activity, while many of those in the ‘everyday economy’ – the parts of the economy that we all depend on to get on with our lives, such as retail, transport and care - struggle by as the high costs of doing business deters prospective investment. Making the business case for investment in parts of the country that feel the economic tides have turned against them has proved difficult as public investment, including our R&D budget, has flowed disproportionately into the Greater South East, leading private investment to follow. And as the case of Britishvolt shows, investment in new green technologies might offer the potential for a new wave of good jobs in poorer places, but it will require sustained investment from government and private sectors

These are grand challenges to overcome. But any government that is serious about driving growth will need to reflect upon the failure of successive governments to deliver higher business investment in the sectors of the economy and places that have lacked it, and think creatively about how a new approach might deliver this.

Over the coming months CPP will outline what a new approach might look like. Over several papers that each take on a different aspect of the economy, we will explore the barriers that prevent business investment that supports inclusive economic growth and will make practical recommendations for reform. Our first paper will build on previous CPP work on local industrial strategy and recent thinking on university-led industrial clusters, setting out ideas to support investment in high-productivity, high-potential industries based in low-productivity places, and how investment can be translated into wider social value for the local economy. We will also be thinking about how to develop stronger foundations for growth through encouraging greater investment in the everyday economy, as well as how we can make a better business case to enhance our long-term energy security, particularly in the parts of the country with the greatest barriers. Throughout this programme we will demonstrate how bold, imaginative reform can deliver productivity growth, create good jobs, and raise living standards across the nation.

We are excited to see where this work takes us and we look forward to speaking to many of you along the way. If you’d like to discuss any of the ideas outlined here in greater depth, then do get in touch: rmudie@progressive-policy.net