Funding fair growth: taxing wealth

4 July 2023

16 minute read

This essay forms part of CPP’s new programme of work on funding fair growth. Our starting premise is that to stop the UK’s continual economic stagnation and political turmoil, a new approach to delivering economic growth is needed, based on public service investment and reform, interventionist industrial strategy and more devolved powers for local government.

The UK’s creaking public services, stagnating health, productivity and earnings have combined with rampant spatial inequalities to create a strong sense that the country is crumbling. But turning the tide will require serious public investment. Stemming the outflow of NHS and school workers, fixing and then expanding childcare, improving adult education, reducing vast geographic inequalities in capital investment, adapting industries and infrastructure to net zero – none of this can be done on the cheap.

In this context, this essay explores wealth taxation as a way of equitably funding fair growth and develops some plausible options for reform.

Context: why tax wealth?

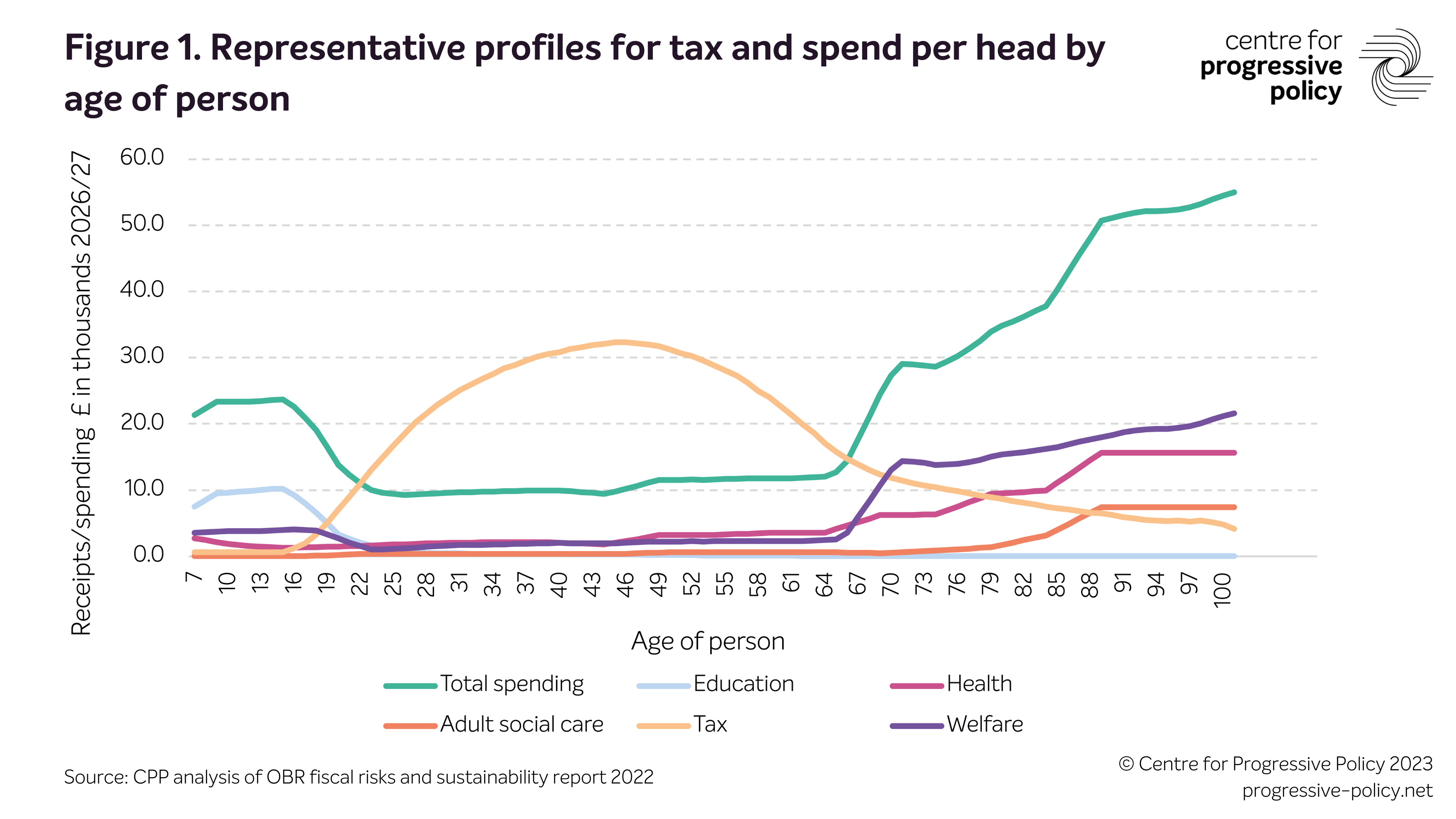

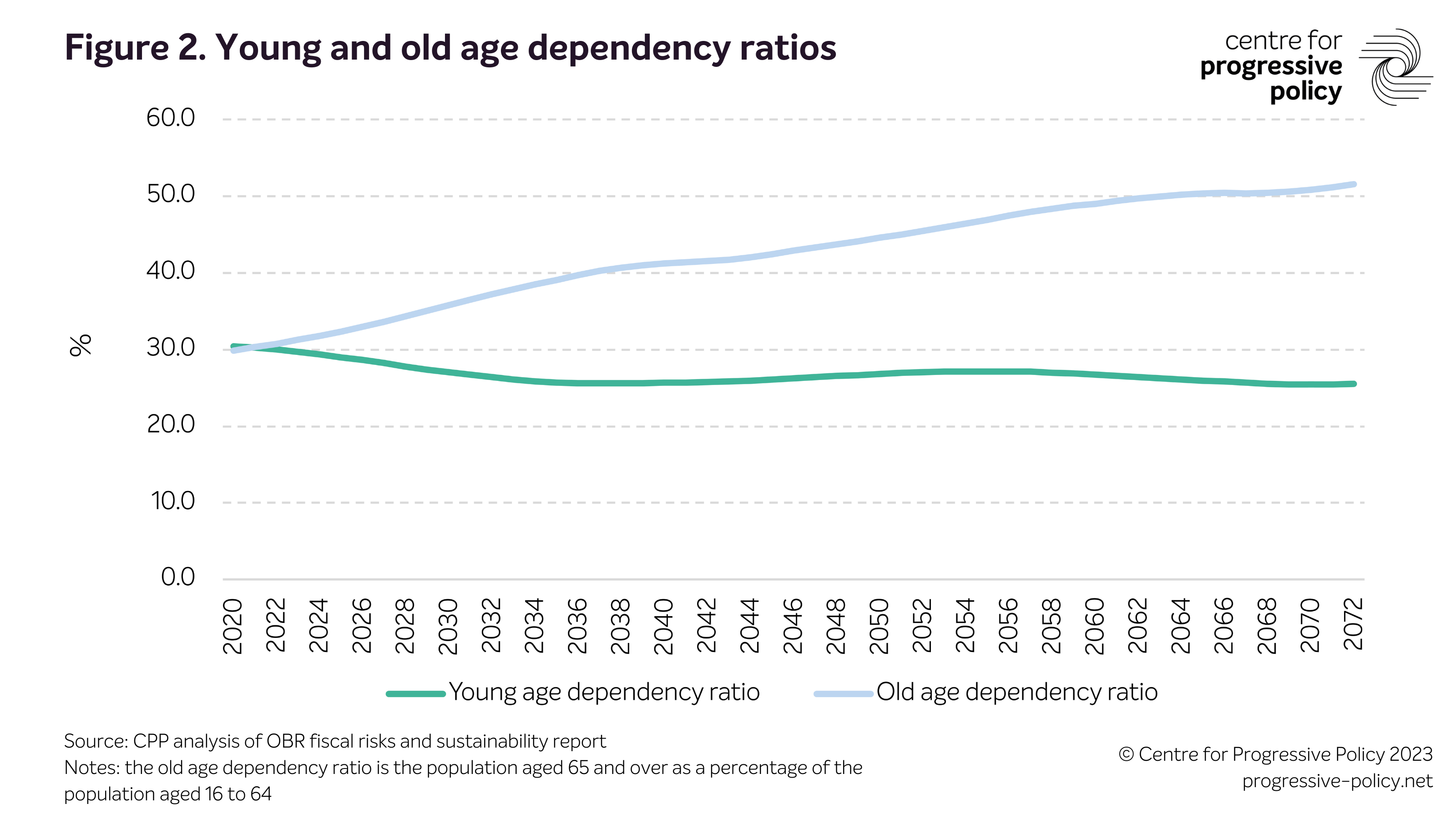

The UK relies heavily on taxing working age people. Every year the UK’s official economic forecaster, the Office for Budget Responsibility, produces a chart showing a representative profile of tax and spend by single year of age. Based on current policy, tax revenues peak when people are in their 40s and spending rapidly overtakes tax revenue after age 65. This is fine when the working age population is growing relative to the older population, but the proportion of the population above working age is now rising the fastest. The old age dependency ratio is set to rise from 30% today to around 45% by 2050. This is likely to increase pressure on the public finances as the revenues from incomes of workers will shrink relative to the spending on healthcare and pensions for older people.

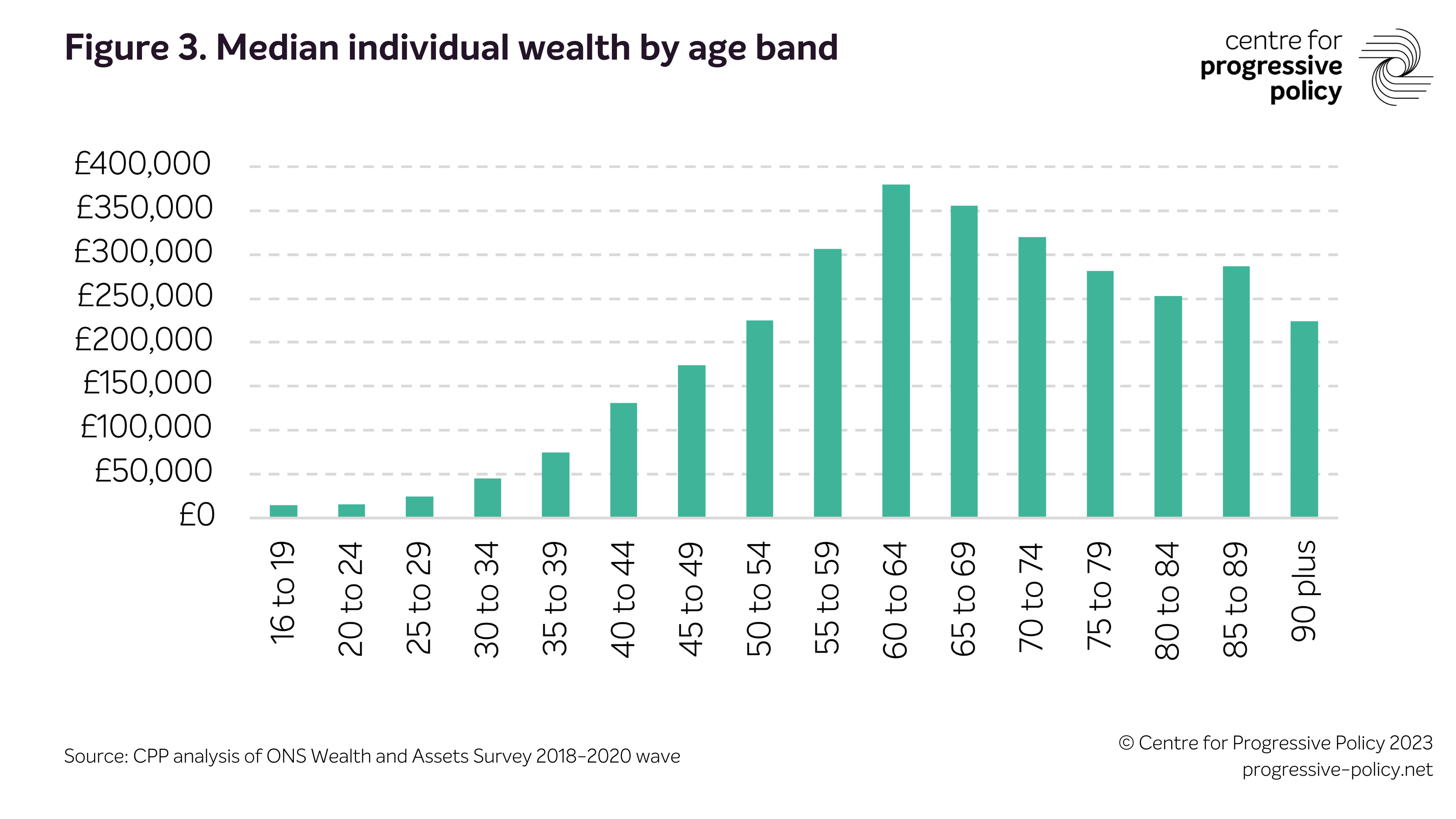

Wealth is much more concentrated at older ages than younger ages, with median wealth for individuals aged 60-64 nine times as high as those in the 30-34 age group. [1] To some extent this is to be expected as wealth accumulation peaks before someone exits the workforce before falling as they consume their wealth once out of work. But even for those significantly beyond State Pension Age (aged 75-79) wealth is still six times as high as the younger age group. By taxing wealth more, public spending could be more sustainable while helping to limit the tax liability of current and future workers.

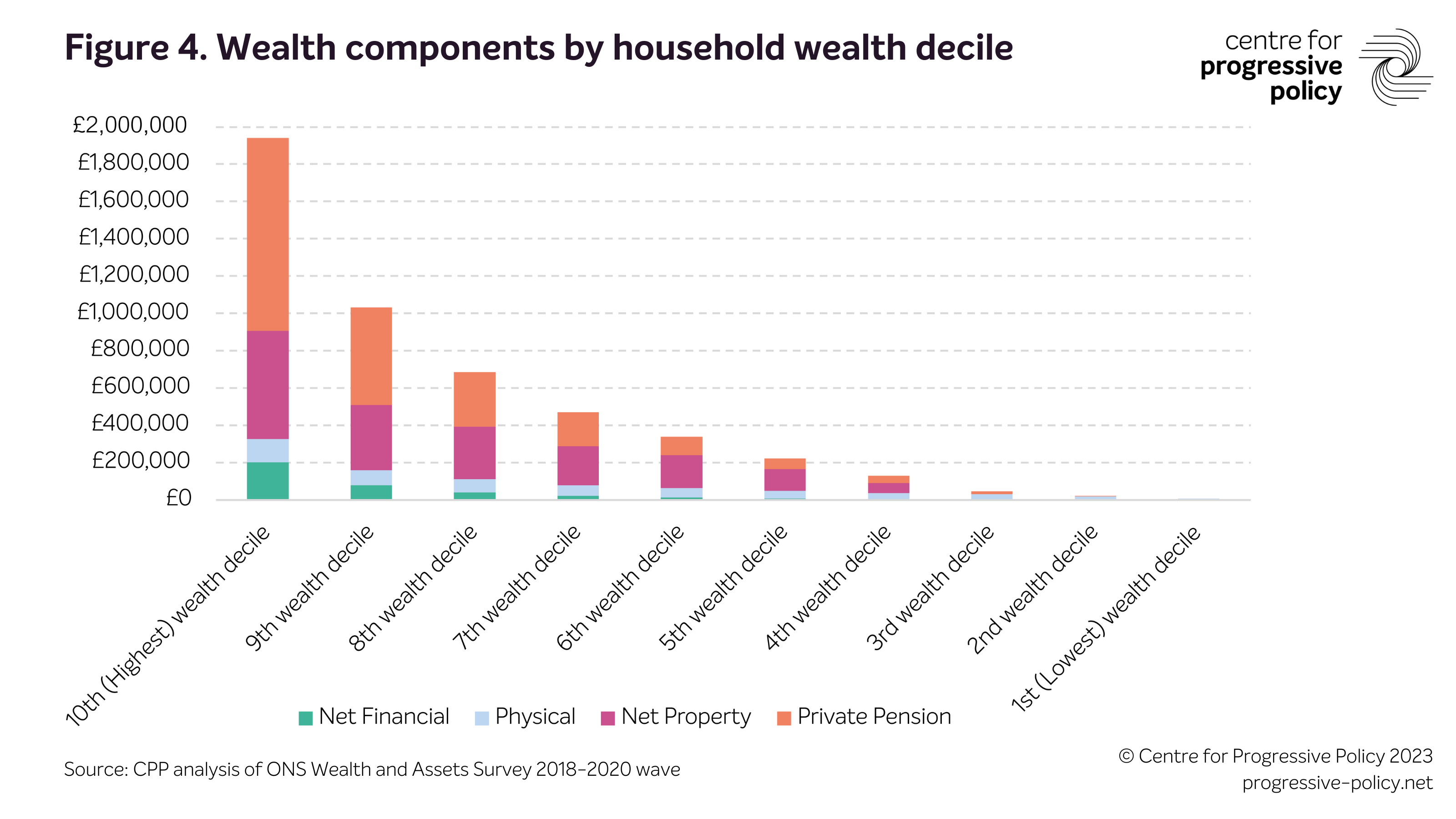

While income taxes are broadly progressive, thereby helping to reduce income inequality, there is no equivalent regarding the treatment of wealth. In the period 2018-2020, the wealth of the richest 1% of households was more than £3.6 million per household, compared to £15,400 or less for the least wealthy 10%. [2] While physical assets were the main component of wealth for the least wealthy, pension wealth was the largest for the wealthiest and property was the largest for those in the middle (see Figure 4).

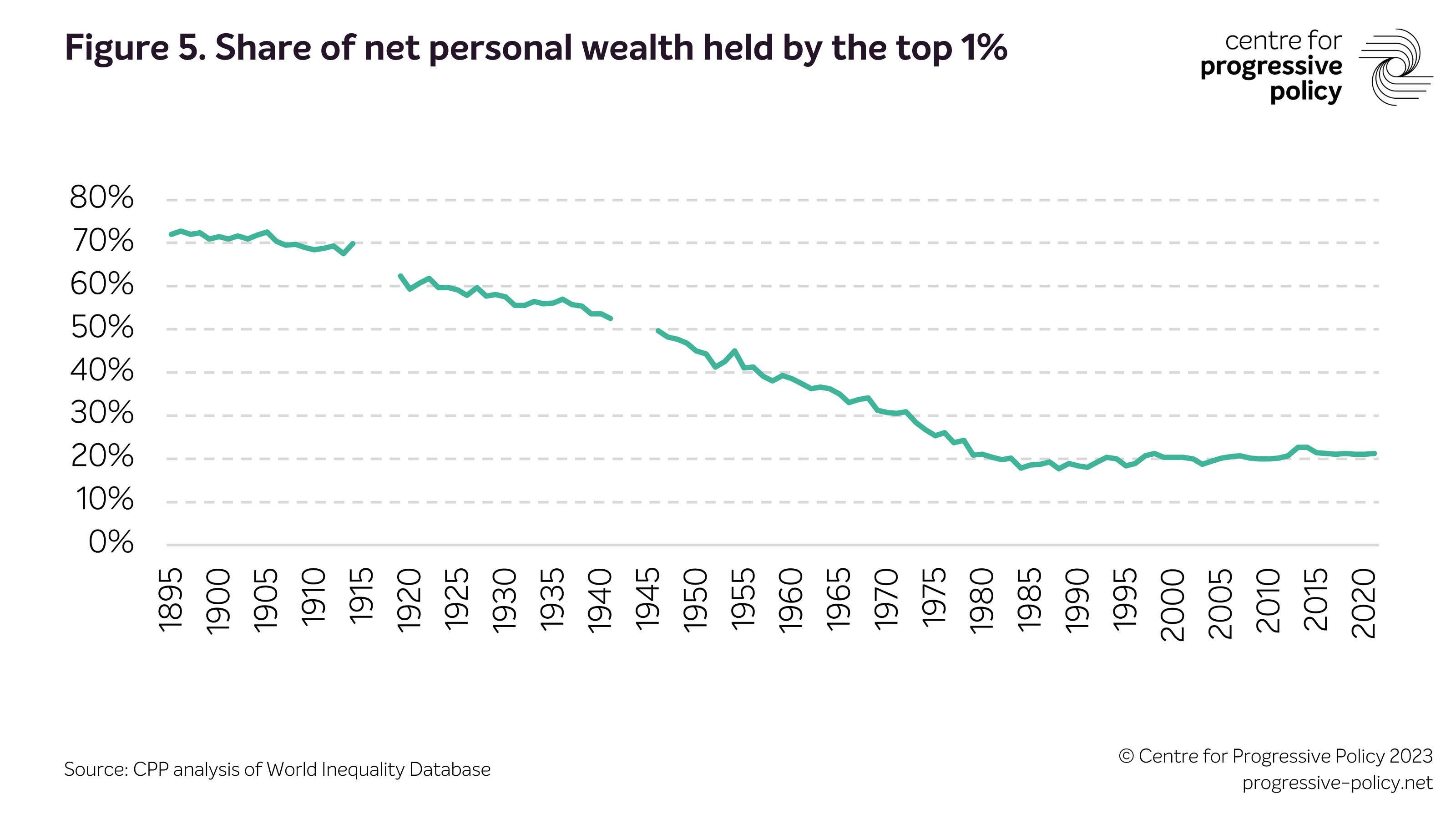

Wealth inequality is significantly greater than income inequality, but the level of wealth inequality has been broadly stable for decades and is much lower than it was in the middle part of the twentieth century (see Figure 5). On this basis a wealth tax is difficult to justify purely on the grounds of preventing an inexorable rise of wealth inequality. Instead the strongest line of argument in favour of taxing wealth is the seemingly unfair and potentially unsustainable treatment of incomes and wages – which are the product of labour and heavily taxed - and wealth – the value of which is mainly not taxed but which has substantially grown due largely to speculation and luck.

Take housing wealth for instance, where evidence shows rising prices are largely a function of the low interest rate environment since the 1990s. Economist Ian Mulheirn estimates that lower mortgage interest rates – the dominant cost of capital for home owners – explains a 160% real terms rise in prices since 1996. [3] He argues the same may be true for pension wealth – estimating that at least 80% of the recent increases in total pension wealth is attributable to interest rate falls rather than more personal savings. [4]

What wealth to tax? International evidence of success - and failure

If we agree with the premise that wealth should be taxed more for reasons of fiscal sustainability and fairness, then what sorts of wealth taxes might be possible?

One very important consideration is the point at which taxes are levied. Currently UK wealth taxes are levied at the point of transaction – the UK has no history of taxing wealth based on the assumed value of assets.

Net wealth taxes are levied at an individual’s entire net worth rather than a specific proportion of it. It is raised on the basis of valuing assets like property that are yet to be sold and not up for sale. Deriving a net wealth tax is therefore a complicated process because a market value has to be estimated on the basis of some formula rather than driven by buyers and sellers. In addition, wealth taxes are tricky to administer – especially for very wealthy individuals who are more likely to have the means to avoid them.

Reporting in 2020, the LSE Wealth Commission recommended a one-off wealth tax for the UK on millionaire couples paid at 1% a year for five years which they estimated would raise £260 billion or £52bn per annum (which is about 2% of GDP). The authors argued that by making a wealth tax one off, it would not deter economic activity or be easily avoided, and would have low administration costs. [5] Making it one-off also avoids the need to regularly value the presumptive gains on assets (i.e. the assumed value of assets today using some agreed definition and metrics) – something which makes taxing net wealth so tricky.

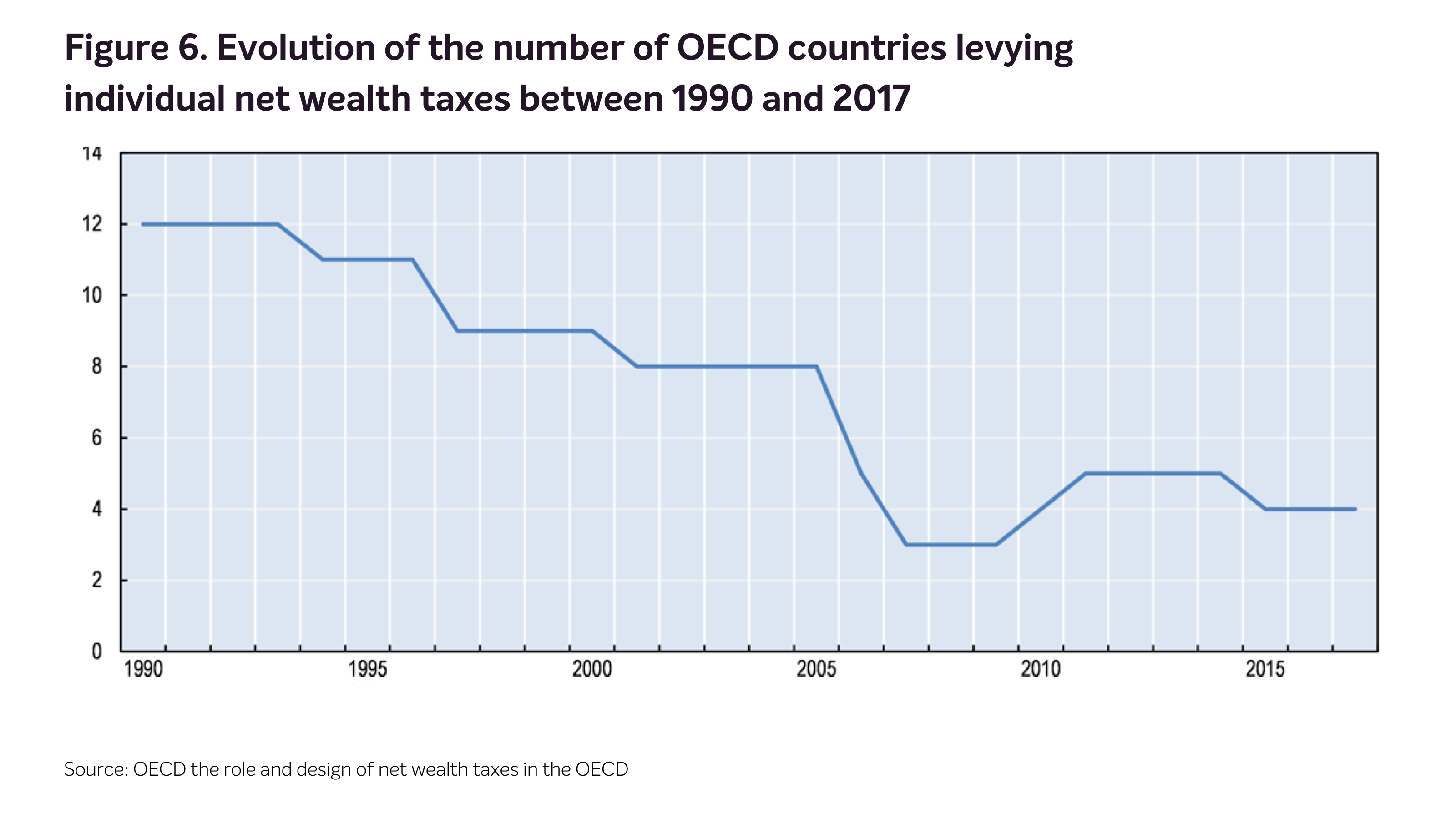

Evidence from abroad suggests little success in levying regular net wealth taxes. The number of countries that operate such taxes has steadily declined from 12 in 1990 to just 4 in 2019 (see Figure 6). The reason for the reduction in countries levying net wealth taxes is twofold. First, they have fallen in favour due to the increased ease with which wealthier individuals can move capital and have access to tax havens meaning they can avoid net wealth taxes altogether. Second, the repeal of net wealth taxes has been part of a more general trend towards lowering tax rates on top income earners. [6] The LSE Wealth Commission reported that in countries where annual net wealth taxes exist, around 7–17% of the initial tax base is lost due to avoidance. [7]

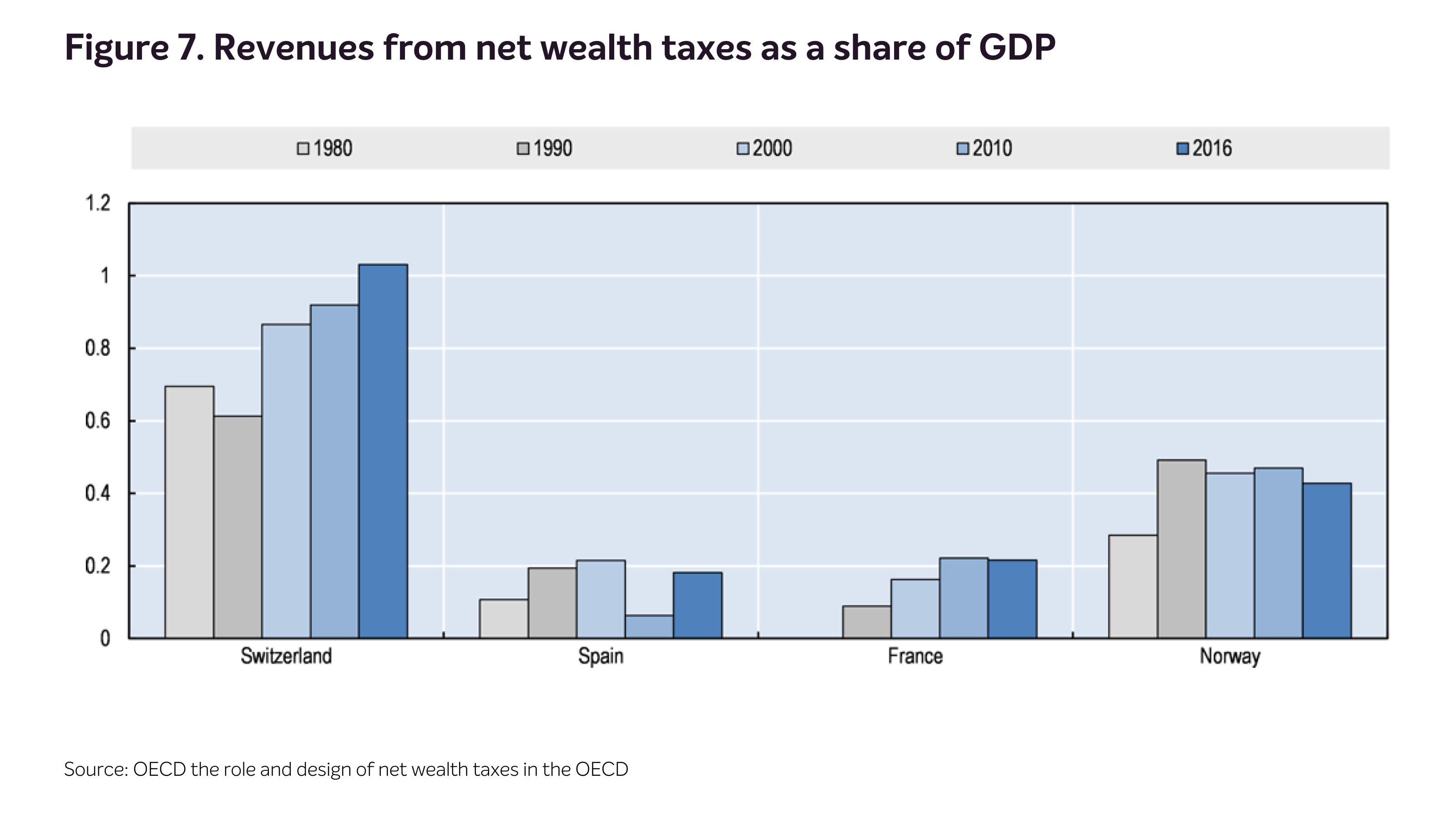

Of those countries that do operate net wealth taxes, they fail to bring in substantial tax revenue – Switzerland manages to raise the highest amount but this is only about 1% of GDP. In Norway it raises less than 0.4% (see Figure 7). These numbers represent a tiny fraction of the overall tax base – tax is around 30% of GDP or higher for most developed countries.

Credible options for taxing wealth in the UK

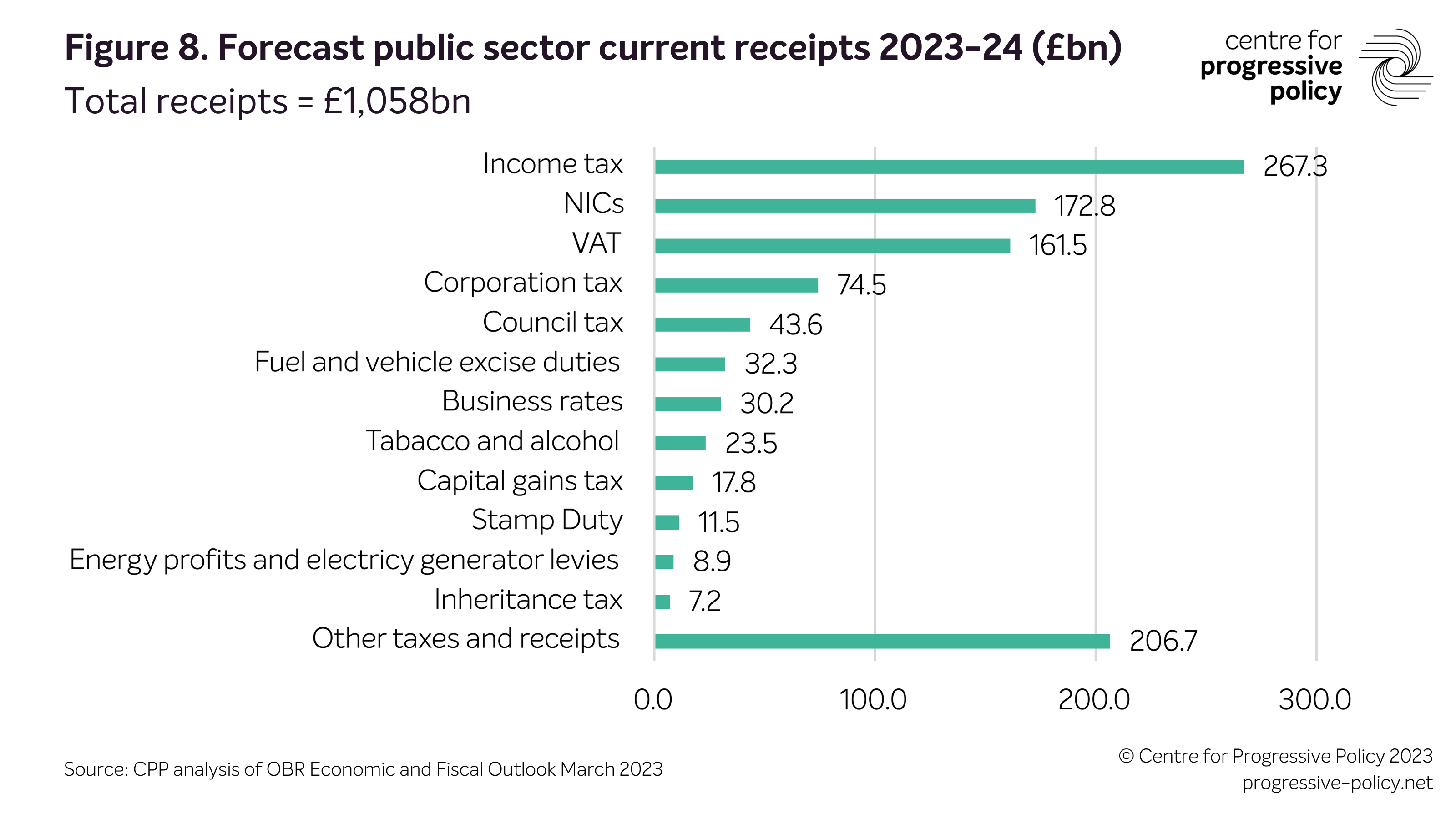

While a one-off net wealth tax might take some time to work out, there is lots that can be done more rapidly. The UK already taxes some forms of wealth at the point of transaction. Capital gains tax is the largest, it is levied on profits made by the sale of assets and is expected to raise about £17.8bn or 1.7% of all tax receipts in 2023-24. [8] Property transaction taxes including stamp duty and land transaction taxes are expected to raise about £12.6bn or 1.2% of tax receipts. Finally, inheritance tax is forecast to raise about £7.2bn or 0.7% of all receipts. [9] Taken together, UK taxes on wealth will amount to about £38bn or 3.6% of total tax revenue. By comparison, taxes on personal income (income tax and national insurance) amount to around £440bn or 42% of tax revenue.

There are many voices urging reform to current UK wealth taxes. Take capital gains for instance, where many organisations have called for capital gains to be taxed in a similar way to incomes. Currently, for higher rate taxpayers, capital gains are taxed at 20 per cent on most assets (non-residential property), and 28 per cent on property including second homes (primary residences are exempt). There are also numerous and complex reliefs including one that specifies any capital gains are written off at death and inheritors then selling assets will only need to pay tax on the capital gains achieved since they inherited the asset. This provides an incentive for people to hold onto assets until death. Finally there is a personal allowance of £6,000 before any tax must be paid on capital gains. All this means that while over 30 million people pay income tax, fewer than 300,000 people pay capital gains tax every year. [10] And of those who paid it over an 11 year period, the vast majority (70%) only paid it once. [11]

Yet the treatment of capital gains was not always so generous. Under Conservative Chancellor Nigel Lawson, capital gains were taxed at the same rate as income tax – with a top rate of 40%. [12] The Office for Tax Simplification has argued that capital gains and income taxes should be treated similarly. [13] They argued that the rate disparity between income tax and capital gains means that:

“…it creates an incentive for taxpayers to arrange their affairs in ways that effectively re-characterise income as capital gains. Most gains are concentrated among relatively few taxpayers, who also tend to have more flexibility about when they dispose of their assets. This can mean that they pay proportionately less tax on their overall income and gains than others.” [14]

In their recent report on tax planning, Resolution Foundation argued that “reasonable people can disagree on how high the tax rates on income should be, but should agree they should be consistent with different forms of income”. [15]

Taxing capital gains and income the same could raise around £10bn per annum although the exact number depends on behavioural change in response to policy reform and whether tax is levied on real or nominal gains. Abolishing the different reliefs on those that can afford to hold assets until death, the large amount that can be earned before any tax is owed, and the reliefs for small business owners selling up and exiting the market could raise double this. [16] Reforming capital gains, would, on the face of it appear relatively low hanging fruit for a government looking raise revenue in a fair way that does not adversely impact economic activity. [17]

Inheritance tax is another area where there are strong advocates for reform. Currently very few people actually pay this tax. It is levied on the value of someone’s estate when they die and charged at the rate of 40% on the value of estates worth over £325,000. But there are several exemptions including any bequests to spouses or civil partners and an allowance on the value of a main residence up to £175,000. In practice, this means inheritance tax might not be due on the first £500,000 of an estate while couple estates will only be taxed if worth more than £1,000,000. All of this means only a small minority of estates at death are eligible for inheritance tax (about 4% in 2020-21, see Figure 9). [18]

Inheritance tax typically evokes an unpopular reaction amongst the public – not just in the UK but around the world. Part of its unpopularity stems from the fact that wealthier individuals and households are better able to avoid paying it altogether than more modestly wealthy households. [19] It is true, for instance in the UK, that inheritance tax is entirely avoidable by timing the transmission of wealth from one family member to another seven years before death. Similarly other exemptions can be easily used to avoid inheritance tax – for instance the business relief exemption means shares invested in the Alternative Investment Market (an unregulated submarket of the London Stock Exchange) will avoid inheritance tax entirely. [20] Agricultural relief means that farmland is also exempt – which has led rising demand and higher prices. [21]

In a recent Demos survey, 55% of the public said inheritance should always be completely tax free in a general sense. However, the principle of taxing the wealth of estates does garner some public support. The same survey found the median response for where people think the tax-free inheritance threshold should sit is around £300,000 (smaller than the existing threshold). [22] Their study also found that the public is, in principle, more accepting of inheritance taxes levied on those with high levels of wealth. [23] The problem, of course, is that the current system leads to tax avoidance amongst the very wealthy. Evidence on inheritance tax avoidance is scarce in the UK and abroad, with estimates from the US suggesting it could be between 8-13% of the overall tax liability. [24]

“The amount that can be inherited tax-free is roughly equivalent to a lifetime of low or middle income work.” [26]

In terms of reforming inheritance tax – two areas are worth exploring further. First is to shift the UK from a system of inheritance tax to one of lifetime gifts. Such a system means levying tax on the recipients of gifts rather than donors’ estates. The UK is one of only three OECD countries that still levies inheritance tax on estates which increases the chance of avoidance. [27] It is possible to transition from one system to another as Ireland has recently shown. The authors of a recent cross-national study on inheritance tax argue that moving to a lifetime receipts-based system does not require heavy technical adjustments, as long as the system is able to record individuals’ gifted wealth over time. [28]

The Resolution Foundation has previously called for a lifetime Receipts Tax. The report’s authors argue that beyond a £125,000 Lifetime Receipts Tax Allowance, a basic rate of 20 per cent should apply, with a top rate of 30 per cent (paid by relatively few) above £500,000 of lifetime receipts. They estimate such a system would bring in about £7bn more per annum over the course of this decade. [28] Such an approach to taxing wealth would help to reduce the ability of avoidance on the part of the wealthy, while continuing to set a sizeable threshold before tax would need to be paid on gifts. In polling by Demos exploring the public’s attitudes to a lifetime gifts tax, 56% of people said £50,000 or less should be tax-free and only 22% said no tax should be paid on gifts of any sort. [29]

Another proposal is to include more assets within inheritance tax. The IFS have argued that pension assets should also be included in inheritance tax – a move that would raise between £0.9bn and £1.9bn per annum within the parameters of the current system. [30] This would mean including the value of any left over pension fund(s) within someone’s estate that is eligible for inheritance tax – currently pensions are exempt from IHT, and if an individual dies before age 75, remaining funds are also exempt from income tax. The IFS argue that pensions are increasingly being used as a vehicle for tax-efficient bequests – which as outlined above is likely to add to the sense of unfairness about wealthier households avoiding it while more modestly wealthy households get caught up.

Conclusion

Taken together, reforms to capital gains and inheritance could, based on conservative assumptions, raise in advance of £20bn additional tax revenue every year. This is substantially more than the commonly offered proposals to raise revenue by abolishing the non-dom tax regime (£3.2bn) [31] or by forcing private schools to charge VAT on pupil fees (£1.6bn). [32] Yet the country may yet need to raise more revenue given the continuing dire state of public services and the desire for a muscular state that drives improvements in fair growth everywhere. For this reason, a one off wealth tax should not be ruled out. Indeed, even if the LSE’s wealth tax only ran for one or two years rather than the proposed five, it could still raise around £50bn – enough to make a significant dent in Labour’s Green Prosperity Plan or to deliver a step-change in the delivery of childcare across the UK.

In our ongoing funding fair growth project, we will be exploring some of the options for taxing wealth with members of the public to come to a judgement on what approaches are most politically feasible and how they might attract broad based appeal.

Notes

[1] https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/distributionofindividualtotalwealthbycharacteristicingreatbritain/april2018tomarch2020

[2] https://obr.uk/docs/dlm_uploads/Fiscal_risks_and_sustainability_2022-1.pdf

[3] https://housingevidence.ac.uk/wp-content/uploads/2019/08/20190820b-CaCHE-Housing-Supply-FINAL.pdf

[4] https://medium.com/@ian.mulheirn/where-did-all-that-wealth-come-from-d9e698bfd477

[5] https://www.lse.ac.uk/News/Latest-news-from-LSE/2020/L-December/Wealth-Commission-report

[7] Assumes a net wealth tax of 1% of assets https://www.lse.ac.uk/International-Inequalities/Assets/Documents/OLDWealthTaxCommission-Final-reportold.pdf

[9] Ibid

[11] Ibid

[12] https://www.ippr.org/files/2019-09/just-tax-sept19.pdf

[13] https://www.newstatesman.com/spotlight/2021/09/fix-the-taxation-of-capital-gains

[14] https://www.gov.uk/government/publications/ots-capital-gains-tax-review-simplifying-by-design

[15] https://economy2030.resolutionfoundation.org/wp-content/uploads/2023/06/Tax_planning.pdf

[16] https://www.ippr.org/files/2019-09/just-tax-sept19.pdf

[17] A point made here: https://www.newstatesman.com/spotlight/2021/09/fix-the-taxation-of-capital-gains

[18] https://ifs.org.uk/publications/death-and-taxes-and-pensions

[20] https://www.resolutionfoundation.org/app/uploads/2018/05/IC-inheritance-tax.pdf

[21] Ibid

[22] https://demos.co.uk/wp-content/uploads/2023/06/the-inheritance-tax-puzzle-final-june-2023-demos.pdf

[23] Ibid

[24] OECD (2021) Inheritance tax in OECD countries https://nuestrosimpuestos.cl/cms/wp-content/uploads/2021/06/OCDE-IMPUESTO-HERENCIA-2021.pdf

[25] https://www.resolutionfoundation.org/app/uploads/2018/05/IC-inheritance-tax.pdf

[28] Ibid

[29] https://demos.co.uk/wp-content/uploads/2023/06/the-inheritance-tax-puzzle-final-june-2023-demos.pdf

[30] https://ifs.org.uk/publications/death-and-taxes-and-pensions

[32] https://www.independent.co.uk/news/uk/politics/keir-starmer-labour-private-schools-b1927130.html